All Land

Discover the latest land for sale

Beranang, Semenyih Residential Land

Beranang, Semenyih

RM 191,664,000

Listed on June 25, 2026

jalan 3/52, seksyen 3, bandar baru bangi

Jalan 3/52, Seksyen 3, Bandar Baru Bangi

RM 1,400 /month

Listed on June 20, 2026

(Bumi Lot - For Bumiputera Buyer only) Bukit Changgang, Tanjong Dua Belas, Banting, Selangor

Bukit Changgang, Tanjong Dua Belas, Banting, Selangor

RM 2,500,000

Listed on May 18, 2026

(Bumi Lot - For Bumiputera Buyer only) Bukit Changgang, Tanjong Dua Belas, Banting, Selangor

Bukit Changgang, Tanjong Dua Belas, Banting, Selangor

RM 2,500,000

Listed on May 15, 2026

(Bumi Lot - For Bumiputera Buyer only) Bukit Changgang, Tanjong Dua Belas, Banting, Selangor

Bukit Changgang, Tanjong Dua Belas, Banting, Selangor

RM 2,500,000

Listed on April 28, 2026

Jalan Bangi Lama, Sg Purun, Semenyih

Jalan Bangi Lama, Sg Purun, Semenyih

RM 19,166,400

Listed on April 28, 2026

Jalan Bangi Lama, Sungai Purun, Semenyih

Jalan Bangi Lama, Sungai Purun, Semenyih

RM 191,664,000

Listed on April 28, 2026

PJ Jalan Profesor Main Road Frontage Land For Sale

PJ Jalan Profesor Main Road Frontage

RM 7,500,000

Listed on April 23, 2026

![[REBUILD POTENTIAL] 4,500sf Flat Land Bungalow @ Seksyen 1, PJ Old Town photo](https://atlasproduction.s3.amazonaws.com/images/subsales/image/941400/medium/e7ec55775b41d23eb52cd5938c671c87bf7ba7ad.jpeg?1773643057)

[REBUILD POTENTIAL] 4,500sf Flat Land Bungalow @ Seksyen 1, PJ Old Town

Seksyen 1, PJ Old Town

RM 880,000

Listed on March 16, 2026

Perdana Hills, Presint 11, Bandar Putrajaya

Jalan P11 A 6/1, Presint 11, 62300 Putrajaya, Wilayah Persekutuan Putrajaya

RM 1,250,000

Listed on November 21, 2025

Presint 8 Bandar Putrajaya

Jalan P8, Presint 8, 62000 Wilayah Persekutuan Putrajaya, Putrajaya

RM 1,400,000

Listed on November 20, 2025

Permatang Tok Gelam, Seberang Perai Utara

Permatang Tok Gelam, Seberang Perai Utara

RM 485,000

Listed on November 4, 2025

Learn

Tips and Guides

LRT3 Shah Alam Line: Stations, TOD & Property Guide 2026

LRT3 Shah Alam Line: Stations, TOD & Property Guide 2026

TL;DR: LRT3 Shah Alam Line at a glance> Opened 29 June 2026, running 37.8 km from Bandar Utama to Johan Setia with 20 stations.Free rides for everyone until 31 July 2026, feeder buses included.> After that, reported fares run up to about RM4.90 cash, RM4.30 cashless and RM2.40 concession.> Serves around 2 million residents. Target ridership is 67,000 a day, rising to 117,708 within five years.> Interchanges: Bandar Utama (MRT Kajang Line) and Glenmarie 2 (LRT Kelana Jaya Line).> The government is planning TOD (affordable housing and shops) on Prasarana land near several stations.> Property tip: transit premiums usually appear 12 to 24 months after a line stabilises, not on launch day. It finally happened. After more than a decade of construction and a long string of delays, the LRT3 Shah Alam Line opened to the public at 6am today, 29 June 2026. Prime Minister Datuk Seri Anwar Ibrahim officiated the launch a day earlier at the Johan Setia depot in Klang. For the western Klang Valley, this is a big deal. Shah Alam and Klang have leaned on cars for decades. Now they finally have a proper rail link. And there is a sweetener. Rides are free for the first month, from today until 31 July 2026. If you live, work, or are thinking of investing along the Petaling Jaya to Shah Alam to Klang stretch, here is everything you need to know. We will also cover the part most headlines skip: Transit-Oriented Development (TOD), the economic ripple effect, and what the line really means for traffic. Everything You Should Know About the LRT3 Shah Alam LineWhat is the LRT3 Shah Alam Line?How many stations does the LRT3 have?What are the LRT3 Shah Alam Line stations?How much are LRT3 fares?Which lines does the LRT3 connect to?What is Transit-Oriented Development (TOD)?TOD Along the LRT3 Shah Alam LineHow the LRT3 Can Boost the EconomyHow the LRT3 Eases Traffic CongestionBest Areas to Invest Around the LRT3 Shah Alam LineThe Future of the LRT3 Shah Alam LineFAQs What is the LRT3 Shah Alam Line? The LRT3, also known as LRT Laluan Shah Alam, is the Klang Valley's third LRT line. It runs 37.8 km from Bandar Utama in Petaling Jaya to Johan Setia in Klang. The line is fully automated and driverless, running on Grade of Automation 4 (GoA4) technology. The trains are the new sky-blue 3-car sets built by CRRC Zhuzhou. Most of the track is elevated. Only one short stretch of about 2.5 km, between Persiaran Dato' Menteri and Stadium Shah Alam, runs underground. The project cost about RM16.63 billion. It was a long road. Construction began in 2016, paused in 2018 for a cost review, then revived and repeatedly delayed before today's opening. How many stations does the LRT3 have? Twenty stations are open at launch. Another five stations (Tropicana, Raja Muda, Temasya, Bukit Raja and Bandar Botanik) are provisional. These were shelved during the 2018 cost-cutting exercise and later reinstated. Construction is expected to begin at the end of 2026. What are the LRT3 Shah Alam Line stations? Here are all 20 stations, grouped by zone from Petaling Jaya down to Klang. ZoneStations (in order)Petaling JayaBandar Utama (interchange, MRT Kajang Line), Kayu Ara, BU 11, Damansara Idaman, SubangShah AlamGlenmarie 2 (interchange, LRT Kelana Jaya Line), Kerjaya, Stadium Shah Alam, Dato' Menteri, UiTM Shah Alam, Seksyen 7 Shah AlamKlangBandar Baru Klang, Pasar Klang, Jalan Meru, Jambatan Kota, Taman Selatan, Seri Andalas, Klang Jaya, Bandar Bukit Tinggi, Johan Setia How much are LRT3 fares? Rides are free for the first month, until 31 July 2026. After that, fares follow the standard distance-based Rapid KL pricing. Reported figures run up to about RM4.90 by cash and RM4.30 cashless, with concession fares around RM2.40. For a daily commuter from Klang or Shah Alam, a cashless fare each way works out to roughly RM189 a month. That can beat petrol, tolls and parking combined. Fares are integrated across the LRT, MRT and Monorail, so you tap once and transfer. Do confirm the latest fares with Rapid KL, as final pricing may be adjusted. Which lines does the LRT3 connect to? Two interchange stations plug the LRT3 into the wider rail network. Bandar Utama connects to the MRT Kajang Line, which runs to Pusat Bandar Damansara, Semantan, TRX and KL Sentral. Glenmarie 2 connects to the LRT Kelana Jaya Line, which serves Bangsar South, Mid Valley (via Abdullah Hukum), KLCC and KL Sentral. Jambatan Kota also sits near the Klang KTM Komuter station for an onward KTM link. So commuters from Klang and Shah Alam finally have a one-transfer ride into KL's main office belts. Feeder buses, vans and parking The line is backed by 40 feeder buses across 13 routes and 323 stops, at RM1 per ride from 6am to 11.30pm. These are also free during the launch month. There are also 44 Rapid On-Demand vans serving 20 zones at RM2 per trip. For drivers, around 2,300 park-and-ride bays are available at the Kayu Ara, Damansara Idaman, Pasar Besar Klang, Seri Andalas, Bandar Bukit Tinggi and Johan Setia stations. What is Transit-Oriented Development (TOD)? Here is where it gets interesting for property. Transit-Oriented Development, or TOD, is the idea of building homes, shops and offices tightly around a transit station. The goal is simple. Put daily life within a short walk of the train, so people drive less and the land around the station actually gets used. A good TOD blends residential, retail and workspace. It puts walkability, covered links to the station and amenities ahead of car parks. Done well, a TOD turns a station from a place you pass through into a place you live, work and spend. TOD Along the LRT3 Shah Alam Line This is now official policy, not just theory. At the launch, the Transport Ministry confirmed it is eyeing several LRT3 station sites for TOD. The named areas include Seri Andalas, Kayu Ara, Bandar Bukit Tinggi and Johan Setia. Transport Minister Anthony Loke made a sharp point. A park-and-ride with 600 bays only ever serves 600 cars a day, because they sit there from morning to night. That land, he argued, can do far more. Prime Minister Anwar pushed the same message. He wants Prasarana's landbank near stations turned into people's housing, not luxury towers, with small shops and stalls for local entrepreneurs. He set an ambitious target: complete affordable, transit-linked housing in Shah Alam within two to three years. The private sector is already moving, with TOD-style projects rising near LRT3 stations and covered walkways planned direct to the platforms. How the LRT3 Can Boost the Economy A new rail line is not just about getting to work faster. It moves money too. First, jobs. The construction phase alone created around 2,000 jobs. Operations, retail and the planned TOD projects will add more. Second, small business. TOD shop lots and stalls give SMEs ready footfall. A station serving tens of thousands of daily riders is a captive market for food, services and convenience retail. Third, land value. When access improves, land near stations becomes more productive. Homes, offices and retail can all command higher value over time. Fourth, spending power. When a household swaps a car loan, petrol and tolls for a roughly RM4 train ride, that saved money gets spent elsewhere in the economy. And there is a wider unlock. Two million residents along the corridor gain easier access to jobs, universities like UiTM Shah Alam, and hospitals like Hospital Tengku Ampuan Rahimah. Better access to opportunity is an economic multiplier in itself. How the LRT3 Eases Traffic Congestion Anyone who drives the Federal Highway or KESAS at rush hour knows the pain. The western corridor has relied almost entirely on roads for decades. Shah Alam and Klang were built around the car. The LRT3 changes the maths. It can move up to 18,630 passengers per hour in each direction. Every full train is dozens of cars taken off the road. Prasarana is targeting 67,000 riders a day in year one, rising to 117,708 within five years. If even a portion are former drivers, the highways breathe a little easier. The line also feeds big traffic generators directly. The Stadium Shah Alam station, for example, gives event crowds a rail option instead of flooding the roads. A realistic note though. Congestion relief is gradual. It builds as ridership grows and as feeder buses and TOD make the train the easy default, not a one-off trip. Best Areas to Invest Around the LRT3 Shah Alam Line Now the question on every investor's mind. Should you buy near an LRT3 station? History says a transit line can lift nearby property values, often by 10% to 20% over comparable homes further out. But timing matters. That premium usually shows up 12 to 24 months after a line stabilises operationally, not on launch day. Anticipation pricing can run ahead of reality, so it pays to be patient. Not all stations are equal either. It helps to think in three zones. 1. Petaling Jaya stretch (already connected) Stations: Bandar Utama, Kayu Ara, BU 11, Damansara Idaman, Subang. These PJ areas already enjoy MRT, LRT or strong highway access. The LRT3 adds convenience, not a structural shift. Capital upside here is the most modest of the three zones. 2. Shah Alam core (the transformation zone) Stations: Glenmarie 2, Kerjaya, Stadium Shah Alam, Dato' Menteri, UiTM Shah Alam, Seksyen 7. This is the standout. Shah Alam has been car-dependent for decades, so this is its first real rail access. The demand drivers are strong: UiTM's large student population, the stadium, and established residential density. For rental investors, stations like Stadium Shah Alam, Dato' Menteri and UiTM Shah Alam look the most promising in the near term. 3. Klang stretch (the long game) Stations: Bandar Baru Klang, Pasar Klang, Jalan Meru, Jambatan Kota, Taman Selatan, Seri Andalas, Klang Jaya, Bandar Bukit Tinggi, Johan Setia. This zone has the biggest transformation potential, and the most competitive entry prices. It is also where the government's TOD plans are most concentrated. The trade-off is time. This is a longer hold, suited to buyers who can wait for the corridor to mature. New projects to watch Several launches are already marketing their LRT3 access. Alia @ Mori Park by OSK Property is a TOD near the Stadium Shah Alam area, about an 800m walk to the line, with prices reported from around RM270,000 for built-ups of 550 to 958 sq ft. Armani Residence Shah Alam by Armani Group takes a lower-density approach, with larger units of roughly 990 to 1,280 sq ft. Across the Shah Alam stretch, new launches have been entering at roughly RM250,000 to RM450,000. For context, the median home in Klang district sits around RM477,000, or about RM335 per sq ft (NAPIC, 2025). One caution worth repeating. Many of these projects complete in 2027 or 2028. You may service loan progress payments for a while before any rental income arrives, and several projects completing at once can compete for the same tenants. Treat all pricing here as indicative and check current figures before you commit. The Future of the LRT3 Shah Alam Line Today is a starting line, not a finish line. Five more stations (Tropicana, Raja Muda, Temasya, Bukit Raja and Bandar Botanik) are due to begin construction at the end of 2026, widening the line's reach. The bigger story is TOD. If the government and private developers deliver affordable, walkable communities around these stations, the LRT3 becomes more than transport. It becomes a backbone for how the western Klang Valley grows. For buyers and investors, the window is now interesting. Prices often soften around launch and firm up once the line proves itself. Watching the Shah Alam and Klang stations over the next 12 to 24 months could pay off. What say you? Is the LRT3 the nudge that finally gets the western corridor out of its cars? FAQs When did the LRT3 Shah Alam Line open? It opened to the public at 6am on 29 June 2026. Prime Minister Anwar Ibrahim officiated the launch on 28 June 2026. Is the LRT3 really free to ride? Yes. Rides on the LRT3 and its feeder buses are free for one month, from 29 June to 31 July 2026. Normal fares apply after that. How many stations does the LRT3 have? Twenty stations are open at launch, from Bandar Utama to Johan Setia. Five more provisional stations are planned, with construction expected to start at the end of 2026. Which lines does the LRT3 connect to? It connects to the MRT Kajang Line at Bandar Utama and the LRT Kelana Jaya Line at Glenmarie 2. Jambatan Kota also sits near the Klang KTM Komuter station. How much will LRT3 fares cost after the free period? Fares follow the distance-based Rapid KL system. Reported figures run up to about RM4.90 cash and RM4.30 cashless, with concession fares around RM2.40. Confirm current fares with Rapid KL. Is property near the LRT3 a good investment? A station nearby can lift values by around 10% to 20% over time, but the premium usually appears 12 to 24 months after the line stabilises, not on launch day. The Shah Alam core and Klang stretch hold the most upside. What is TOD and why does it matter for the LRT3? TOD, or Transit-Oriented Development, builds homes, shops and offices within walking distance of a station. The government plans TOD on Prasarana land near several LRT3 stations, which could reshape neighbourhoods and property demand. Thinking of buying, renting or investing along the LRT3 Shah Alam Line? Our IQI property professionals know these neighbourhoods inside out. Leave your details below and we will help you find the right home or investment. [custom_blog_form] Continue reading: Damansara Rental Yield for Property Investment 5 Reasons Why You Should Invest in Klang Valley in 2025 3 Reasons Why You Will Definitely Want to Live in Petaling Jaya! | Real Estate 101 Sources & References: Figures in this article reflect official announcements and launch-day reporting as of 29 June 2026. Fares and project details may be revised, so confirm current information with Rapid KL and the relevant developers before making decisions. The Star. (2026, June 27). PM Anwar to launch LRT3 Shah Alam line tomorrow. Tan, D. (2026, June 28). LRT3 Shah Alam Line launched by PM, 20 stations open to public 6am tomorrow, free rides till July 31. Paultan.org. Malay Mail. (2026, June 27). PM Anwar to launch LRT3 Shah Alam Line tomorrow, 20 new stations set to transform commutes. RinggitPlus. (2026, June). LRT3 Shah Alam Line starts operations on 29 June. The Edge Malaysia. (2026, June 28). MOT eyeing several sites around LRT3 stations for transit-oriented housing projects, says minister. Scoop. (2026, June 28). LRT3 launch: Anwar pushes Prasarana land for affordable, people's housing under TOD push. New Straits Times. (2026, June 28). Affordable housing, retail spaces planned along Shah Alam LRT3 line. EdgeProp.my. (2026, June 28). Transport Ministry identifies several areas around LRT3 stations for TOD projects. Hartamas Real Estate. (2026). LRT3 is open: What past rail launches tell us about property prices. EdgeProp.my. (2025, July 2). New home launches around soon-to-start LRT3. Prasarana Malaysia / Rapid Rail. (2026). LRT Shah Alam Line (LRT3). Railway News. (2026, May 17). LRT3 project: 2026 construction update and route map. For the most accurate and up-to-date information, please refer to official announcements from Prasarana and Rapid KL.

Continue Reading

Damansara Rental Yield for Property Investment

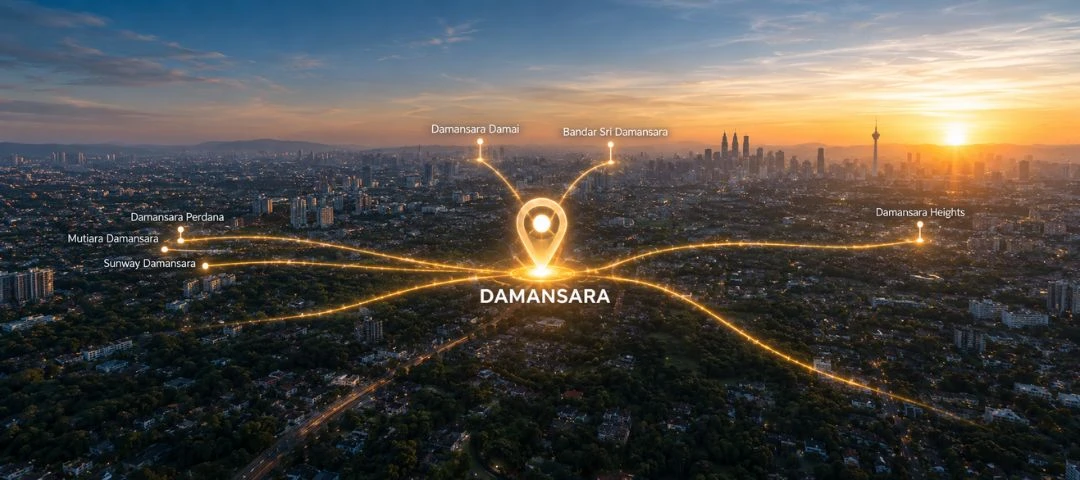

Damansara Rental Yield for Property Investment

TL;DRDamansara rental yield is strongest when you buy the right property type in the right pocket, not just the most famous neighborhood. Based on various data, Damansara Perdana stands out for condo yield, while Sunway Damansara, Damansara Damai, and Bandar Sri Damansara show useful landed-house yield signals. Premium areas such as Damansara Heights and Mutiara Damansara can still be excellent long-term plays, but they are usually more about capital value than easy positive cash flow. Damansara sounds like one neat area, but for investors, it behaves more like a family WhatsApp group: same surname, very different personalities. One pocket offers a higher monthly rent, another protects long-term value, and another looks fancy but makes the yield do push-ups. This guide breaks down Damansara rental yield by area, property type, and tenant demand, so you do not buy with vibes alone. Key Takeaways Damansara Perdana rental yield is one of the clearest condo-yield opportunities, with implied yields of 3.85% and 6.33% for 1,001-1,500 sq ft units in its rental yield table. Sunway Damansara rental yield is a strong landed-house signal, reporting 5.04% for houses, although investors still need to compare the exact property condition, rentability, and entry price. Ara Damansara rental yield depends heavily on property type, with reports showing 2.05% for houses, while one expert places the gross yield for Ara Damansara condos at 4.5% to 5.5%. Kota Damansara rental demand is supported by MRT access, hospitals, schools, universities, malls, and commercial centers. Notably, 2,284 serviced apartments and condominium units are set to enter the market in 2026, which could pressure rents in the near term. Damansara Heights rental yield should be read carefully, as it varies by asset type. One reports 6% implied yield, while the luxury condo gross yield is at 3.0% to 4.0%, and a lower net yield for Damansara Heights by bedroom count. What You Should Know About Damansara Property1. What is the average Damansara rental yield in 2026?2. Which Damansara area has the best rental yield?3. How do you calculate rental yield for a Damansara property?4. Is a Damansara condo or a landed house better for rental income?5. Which Damansara areas have the strongest tenant demand?6. What risks should investors check before buying in Damansara?7. Is Damansara still a good place for property investment?8. Frequently Asked Questions (FAQs) Estimated reading time: 16 minutes 1. What is the average Damansara rental yield in 2026? Damansara rental yield can range from roughly 2% to above 6%, depending on neighborhood, property type, price per square foot, rent per square foot, and whether the yield is gross or net. The safest answer is this: Damansara is not one rental market. It is a cluster of different rental markets across Petaling Jaya and Kuala Lumpur. For example, iRumah reports Damansara Kim's house rental yield at 1.82%, while EdgeProp reports Damansara Kim’s implied rental yield at 2.23%. That difference already tells investors something important: different platforms may use different data pools, timeframes, and property samples. At the higher-yield end, EdgeProp reports Damansara Perdana at 3.85% implied yield, with a 6.33% rental yield for 1,001-1,500 sq ft units in its rental yield table. iRumah also reports Damansara Damai at 4.0% for houses and Sunway Damansara at 5.04% for houses. The practical lesson is simple: do not ask only, “What is the rental yield in Damansara?” Ask, “Which Damansara area, which property type, and at what purchase price?” a. Damansara rental yield comparison table Damansara areaproperty typeRental yield signalKey rental demand driverInvestor readingDamansara PerdanaCondominium/apartment3.85% implied yield; 6.33% for 1,001-1,500 sq ft unitsUrban lifestyle, studios, SOHO, proximity to Mutiara Damansara and PJStrongest condo yield signalSunway DamansaraHouses5.04%MRT, hospitals, universities, schools, Kota Damansara catchmentStrongly landed-house yield signalDamansara DamaiHouses4.0%MRT Damansara Damai, affordable housing baseAffordable entry with traffic caveatBandar Sri DamansaraHouses3.05%MRT, highways, mature township, schoolsStable practical demandDamansara JayaTerrace houses3.16% implied yield; 4.12% for 1,501-2,000 sq ft unitsMature PJ address, schools, Atria areaBetter yield than some mature landed pocketsAra DamansaraHouses/condos2.05% for houses; 4.5%-5.5% gross for condos (est.)LRT Ara Damansara, Subang, and PJ workforceBetter for condos than landed yieldMutiara DamansaraHouses2.72%MRT, malls, hospitals, and a premium lifestyleMore lifestyle and capital-value drivenDamansara KimTerrace houses1.82% to 2.23%Mature SS20 landed neighborhood, local amenitiesLower yield, mature landed appealDamansara HeightsDetached, semi-detached, terrace, land/luxury condos6% implied yield; 3.0%-4.0% luxury condo gross yieldPrestige, diplomats, legacy wealth, premium rentalsStrong address, yield depends heavily on asset typeSources: EdgeProp, iRumah, PropCashflow.my, Property Genie Data note: These figures are not all directly comparable because some refer to houses, some to condos, and some to broader implied yield. For a clean investment decision, compare similar units in the same building or on the same street, not just by area labels. 2. Which Damansara area has the best rental yield? Damansara Perdana has the strongest condo-yield signal, while Sunway Damansara has the strongest landed-house yield signal in the ingested data. For investors, that split matters because a condo rental and a landed house rental are not the same game. Damansara Perdana works well as a condo rental market because it has smaller units, studios, duplexes, and apartment rooms listed in the rental market, which can support more affordable monthly rent points. EdgeProp reports a median sale price of RM592 psf, a median rental price of RM1.58 psf, and an implied rental yield of 3.85% for Damansara Perdana. Its rental yield table also shows 1,001-1,500 sq ft units with an average monthly rent of RM2,600, an average price of RM497,397, and a rental yield of 6.33%. Sunway Damansara is different. iRumah reports a house rental yield of 5.04%, with house prices ranging from RM1.2 million to RM9.77 million. This makes it a strong landed-house signal, but the wide price range means investors must check whether the rent can really support the purchase price. Damansara Damai also deserves attention for rental income. iRumah reports a 4.0% rental yield for houses, with house market prices from RM760,000 to RM2.1 million. The advantage is affordability. The drawback is also stated in the source: peak-hour congestion and limited entry or exit access can affect daily living. a. Best Damansara area by investor goal Investor goalBest-fit areaWhy it fitsHighest condo yieldDamansara PerdanaStrong yield for 1,001-1,500 sq ft unitsStrong landed-house yieldSunway Damansara5.04% yield for housesAffordable landed-house yieldDamansara Damai4.0% yield and lower house entry rangeMature PJ stabilityBandar Sri DamansaraActive transactions and improved infrastructurePremium capital-value playMutiara Damansara, Damansara HeightsStronger lifestyle and prestige profile, but yield must be checked unit by unitTransit-linked condo strategyAra Damansara, Kota Damansara, Damansara PerdanaLRT, MRT, malls, and working populations support tenant demandSource: EdgeProp, iRumah, Brickz, The Edge Malaysia If you want a single clean answer, the best Damansara area for rental yield isn't a single neighborhood. It is the best match between yield, asset type, and tenant profile. For condo yield, start with Damansara Perdana. For landed yield, compare Sunway Damansara, Damansara Damai, and Bandar Sri Damansara carefully. 3. How do you calculate rental yield for a Damansara property? Gross rental yield is calculated by dividing annual rental income by property value, then multiplying by 100. It is the first fast check, but it is not the final investment answer. Use this formula: Gross rental yield = Annual rental income ÷ property value × 100 Let’s say a Damansara condo rents for RM2,600 per month and has an average price of RM497,397. Annual rental income is RM31,200. Using the gross yield formula, the rough result is about 6.3%, which is close to EdgeProp’s reported 6.33% rental yield for Damansara Perdana units sized 1,001-1,500 sq ft. But serious investors should also calculate net rental yield. PropCashflow defines net yield as annual rent minus operating costs, divided by purchase price, and includes costs such as maintenance fees, sinking fund, quit rent, assessment rates, rental income tax, vacancy allowance, and landlord insurance. Bamboo Routes also stresses that net yield matters because service charges, vacancy, repairs, leasing, and other costs reduce the actual return. Use this formula: Net rental yield = Annual rental income after costs ÷ property value × 100 Net rental yield is what remains after the property stops looking pretty on a spreadsheet and starts behaving like real property. Maintenance, repairs, vacancies, and furnishing costs all have a way of joining the party uninvited. 4. Is a Damansara condo or a landed house better for rental income? Damansara condo rental yields are usually easier to optimize than landed-house yields because condos often have lower entry prices, smaller unit sizes, and clearer tenant pools. Landed houses can still be valuable, but they often lean more toward long-term capital appreciation and family use. The clearest example is Damansara Perdana. EdgeProp reports a 6.33% yield for 1,001-1,500 sq ft units, indicating stronger income efficiency for selected condo or apartment stock. iRumah also shows Damansara Perdana rental listings for studios, duplexes, rooms, and shop-offices, suggesting a more varied rental market. For landed houses, results vary widely. iRumah reports rental yields of 2.05% for houses in Ara Damansara, 2.72% in Mutiara Damansara, 1.82% in Damansara Kim, and 3.05% in Bandar Sri Damansara. That does not mean landed homes are bad investments. It means that the Damansara landed house rental yield can be lower because buyers pay for land value, scarcity, neighborhood prestige, and family appeal. These qualities may support resale value, but they do not always push the monthly rental enough to create a high yield. a. Condo vs landed investment logic Property typeBetter forMain advantageMain riskCondo/apartmentRental yield and tenant flexibilityLower entry price and easier furnishing packageBuilding competition and service chargesServiced apartmentShort-term tenants and furnished rentalStrong rental appeal near malls or transitHigher maintenance and possible oversupplyLanded houseLong-term ownership and family tenantsLand value and capital appreciation potentialA higher purchase price can compress the yieldShop-officeCommercial rental incomeCan command higher rent in active commercial areasTenant quality and business-cycle risk For many first-time investors, a furnished condo rental near an MRT or LRT station is the easier starting point. Landed houses suit investors who can accept a lower yield while waiting for long-term capital appreciation. IQI Global can help investors compare both new launches and subsale property options, especially when the choice is not simply “buy where the yield looks highest.” Approach us now for more Damansara property! Find Damansara Property Now! 5. Which Damansara areas have the strongest tenant demand? Tenant demand is strongest where renters have daily reasons to stay: MRT and LRT stations, malls, hospitals, schools, universities, offices, highways, and lifestyle amenities. In Damansara, these points strongly point toward Kota Damansara, Ara Damansara, Damansara Perdana, Bandar Sri Damansara, and selected premium pockets. Kota Damansara has a strong rental story, supported by MRT access, malls, education, healthcare, and commercial centers. Kota Damansara is served by Surian MRT, Kota Damansara MRT, and Kampung Selamat MRT, and has amenities such as The Strand Mall, Sunway Nexis Mall, Sunway Giza Mall, and Tropicana Gardens Mall. According to The Edge Malaysia, working adults and students from nearby universities drive demand for high-rise residential properties. Ara Damansara is another strong area for tenant demand, especially for condos near transit. LRT Ara Damansara, LRT Kelana Jaya, and LRT Lembah Subang are nearby transit stations. PropCashflow places the Ara Damansara condo gross yield at 4.5% to 5.5%, supported by the LRT Kelana Jaya Line, the Subang and PJ workforce, proximity to Subang Airport, and Evolve Concept Mall. Bandar Sri Damansara has a practical occupancy rate story. The Edge Malaysia reports that condominium units and apartments there had 80% to 90% occupancy, while offices, shophouses, and retail shops at Ativo Plaza and 8trium had 70% to 90% occupancy Brickz also reports 215 residential transactions in Bandar Sri Damansara between May 2025 and April 2026, with a median PSF of RM507 and a median property price of RM480,000. Damansara Heights and Mutiara Damansara have different rental demand profiles. They are not mainly affordability plays. Mutiara Damansara is supported by malls, MRT, and premium township planning, while Damansara Heights attracts legacy wealth, diplomats, and premium renters according to Property Genie’s luxury condo comparison. 6. What risks should investors check before buying in Damansara? Investment property decisions in Malaysia should never rely solely on the headline rental yield. In Damansara, investors must check the property type, source of funds, vacancy risk, maintenance costs, new supply, traffic, and whether the quoted yield is gross or net. First, check the new supply risk. Kota Damansara has a strong demand, but The Edge Malaysia reports that in 2024, three ongoing projects will add 2,284 serviced apartments and condominium units over the next two years. More units can give tenants more choices, which may pressure rental growth if supply rises faster than demand. Second, check gross rental yield against net rental yield. A few experts both make the same practical point: gross yield is only the first screen, while net yield must deduct real operating costs. If your condo looks good at 5% gross but has high service charges, long vacancy periods, and heavy furnishing costs, the real return can shrink quickly. Third, check whether the property is leasehold or freehold. For example, Sunway Damansara and Damansara Perdana are leasehold, while Mutiara Damansara is freehold. Tenure alone does not decide investment quality, but it affects buyer perception, financing comfort, and long-term resale confidence. Fourth, check traffic and access. Traffic congestion challenges in Ara Damansara and Damansara Damai, with Damansara Damai facing peak-hour issues because of limited entry and exit access. A renter may love cheap rent, but not if the daily commute feels like a boss fight. Finally, check the property value versus the rental income. Newprojek reports Mutiara Damansara’s median price at RM1.50 million and median PSF at RM868 based on 67 verified transactions from October 2021 to February 2026. iRumah reports Mutiara Damansara house rental yield at 2.72%. That combination suggests investors should treat Mutiara Damansara more as a premium lifestyle or capital-value market than a pure cash-flow play. IQI Global is useful here because investors often need help comparing not just listing price, but also rentability, furnishing strategy, tenant profile, and resale appeal. We can help you with that! Let Us Help You! 7. Is Damansara still a good place for property investment? Damansara property investment remains attractive, but the best strategy is to choose based on the investor's goals rather than chasing a single “best” area. For rental yield, start with Damansara Perdana, Sunway Damansara, Damansara Damai, and Bandar Sri Damansara. For tenant depth, focus on Kota Damansara, Ara Damansara, and Damansara Perdana. For long-term capital preservation, study Mutiara Damansara and Damansara Heights. If you want positive cash flow, you need to be strict. Compare the monthly rent, maintenance fees, vacancy risk, and loan payments before buying. Various pieces of information support a clear pattern: smaller or mid-sized units near transit and amenities are easier to shape into rental investments, while premium landed homes may require a longer holding horizon. If you want capital appreciation, mature and premium pockets can still make sense. Mutiara Damansara shows a median price of RM1.50 million and a +6.4% increase since 2021 on Newprojek’s transaction page. Damansara Heights is repeatedly framed as a prestige and legacy-wealth area by EdgeProp and Property Genie. If you want a balanced property investment, the sweet spot is a property with an acceptable rental yield, strong tenant demand, and realistic resale value. In layman's terms, buy something people actually want to live in, at a price that still makes the rent work. IQI Global can help buyers and investors explore opportunities in Damansara, compare rental demand across neighborhoods, and shortlist properties that align with both income and long-term value goals. Explore Damansara Property Damansara rental yield is not about picking the fanciest name on the map. It is about matching the right property type to the right tenant pool at the right price. Damansara Perdana looks strongest for sourced condo yield, while Sunway Damansara and Damansara Damai show useful landed-house signals. For a safer investment, compare yield, demand, costs, and resale value together. 8. Frequently Asked Questions (FAQs) a. What is the rental yield in Damansara? Damansara rental yield varies by area and property type. The ingested sources show lower house yields in mature landed areas, such as Damansara Kim, while condo-focused areas, such as Damansara Perdana, show stronger sourced rental yield signals. b. Which Damansara area has the best rental yield? Damansara Perdana has the strongest condo-yield signal, with an implied yield of 3.85% and 6.33% for 1,001-1,500 sq ft units. For houses, Sunway Damansara shows a strong sourced yield at 5.04%. c. How do I calculate rental yield for a Damansara property? Rental yield is calculated by dividing annual rental income by property value, then multiplying by 100. For net yield, deduct costs such as maintenance, vacancy, tax, insurance, and repairs before dividing by the property value. d. Is Ara Damansara better than Damansara Perdana for rental income? Ara Damansara is better for LRT-linked professional demand, while Damansara Perdana has a clearer condo-yield signal. Ara Damansara house yields at 2.05%, while Damansara Perdana’s implied yield is at 3.85%, and the selected unit yields at 6.33%. e. Should I buy a condo or a landed house in Damansara for rental income? Condo rentals are usually easier to rent out because entry prices are often lower and tenant pools are broader near transit, malls, and offices. Landed homes in Damansara can still be strong long-term assets, but high property value can reduce yield efficiency. f. Is Damansara Heights good for rental yield? Damansara Heights rental yield depends heavily on asset type. 6% implied yield, but a luxury condo gross yield at 3.0% to 4.0%, and a lower net yield for Damansara Heights by bedroom count. g. What is a good rental yield for property investment in Malaysia? Good rental yield depends on risk, costs and location, not just percentage. PropCashflow ranks many stronger Malaysian urban yield areas around 4.5% to 7.5% gross, while Bamboo Routes stresses that net yield is more important after costs and vacancy. IQI Global can help you compare properties in Damansara based on yield, tenant demand, and long-term value. Explore your next investment with our team today. [custom_blog_form] Continue Reading: Property Overhang vs Unsold Property in Malaysia: What Buyers Must Know What is Debt-To-Service Ratio (DSR) in Malaysia & How It Affects Your Home Loan What Is eSPA? Malaysia’s New Initiative to Help Homebuyers Buy Faster Sources and References Bamboo Routes. (2026, January 13). What rental yield can you expect in Malaysia? (2026). Retrieved fromhttps://bambooroutes.com/blogs/news/malaysia-rental-yields Brickz. (n.d.). BANDAR SRI DAMANSARA, SELANGOR - RESIDENTIAL. Retrieved fromhttps://www.brickz.my/transactions/residential/selangor/bandar-sri-damansara/ Chai, Y. H. (2023, April 13). Rental Market: Bandar Utama terraced houses enjoy strong rental demand. The Edge Malaysia. Retrieved fromhttps://theedgemalaysia.com/node/662066 Chai, Y. H. (2024, June 26). Rental Market: Kota Damansara’s rental market buoyed by strategic location, good amenities. The Edge Malaysia. Retrieved fromhttps://theedgemalaysia.com/node/715384 EdgeProp. (n.d.). Ara Damansara. Retrieved fromhttps://www.edgeprop.my/area-outlook/selangor/ara-damansara EdgeProp. (n.d.). Damansara Heights (Bukit Damansara), Damansara Heights Insights. Retrieved fromhttps://www.edgeprop.my/project/damansara-heights-bukit-damansara--16828 EdgeProp. (n.d.). Damansara Jaya, Petaling Jaya Insights. Retrieved fromhttps://www.edgeprop.my/project/damansara-jaya-14418 EdgeProp. (n.d.). Damansara Kim, Damansara Insights. Retrieved fromhttps://www.edgeprop.my/project/damansara-kim-9391 EdgeProp. (n.d.). Damansara Perdana, Petaling Jaya Insights. Retrieved fromhttps://www.edgeprop.my/condo/damansara-perdana-30168 Hartamas. (2026, March 30). Arra Residences Ara Damansara: An Honest 5-Question Review (2025) - Hartamas Real Estate. Retrieved fromhttps://hartamas.com/arra-residences-ara-damansara-an-honest-5-question-review-2025/ iHome.my. (2026, June 19). Buying or Renting in Damansara 2026: Kota Damansara, Mutiara, TTDI Guide. Retrieved fromhttps://ihome.my/areas/damansara-property-guide/ iRumah. (n.d.). Ara Damansara, Petaling Jaya. Retrieved fromhttps://irumah.co/petaling-jaya/ara-damansara iRumah. (n.d.). Bandar Sri Damansara, Petaling Jaya. Retrieved fromhttps://irumah.co/petaling-jaya/bandar-sri-damansara iRumah. (n.d.). Damansara Damai, Petaling Jaya. Retrieved fromhttps://irumah.co/petaling-jaya/damansara-damai iRumah. (n.d.). Damansara Jaya, Petaling Jaya. Retrieved fromhttps://irumah.co/petaling-jaya/damansara-jaya iRumah. (n.d.). Damansara Kim, Damansara Utama. Retrieved fromhttps://irumah.co/damansara-utama/damansara-kim iRumah. (n.d.). Damansara Perdana, Petaling Jaya. Retrieved fromhttps://irumah.co/petaling-jaya/damansara-perdana iRumah. (n.d.). Damansara Utama, Petaling Jaya. Retrieved fromhttps://irumah.co/petaling-jaya/damansara-utama iRumah. (n.d.). Mutiara Damansara, Petaling Jaya. Retrieved fromhttps://irumah.co/petaling-jaya/mutiara-damansara iRumah. (n.d.). Sunway Damansara, Kota Damansara. Retrieved fromhttps://irumah.co/kota-damansara/sunway-damansara Lee, R. (2026, March 18). Market Pulse: Steady growth keeps Damansara Uptown buzzing. The Edge Malaysia. Retrieved fromhttps://theedgemalaysia.com/node/795321 Newprojek. (2026, January 1). Best Property Investment in Petaling Jaya 2026. Retrieved fromhttps://newprojek.com/guides/best-property-investment-petaling-jaya Newprojek. (n.d.). MUTIARA DAMANSARA Property Value & Price History. Retrieved fromhttps://newprojek.com/property-transaction/mutiara-damansara PropCashflow.my. (2026, February 23). Best Rental Yield Areas in Malaysia 2026: Top 15 Ranked. Retrieved fromhttps://propcashflow.my/blog/best-rental-yield-areas-malaysia-2026-ranked/ Property Genie. (n.d.). Luxury Condo Kuala Lumpur 2026: KLCC, Mont Kiara, Bangsar, TTDI & Damansara Heights Compared. Retrieved fromhttps://www.propertygenie.com.my/insider-guide/luxury-condo-kuala-lumpur-2026-klcc-mont-kiara-bangsar-ttdi-damansara-heights-compared-P5aEk63pS4C4LHerKrVZVh Residential Property KL. (n.d.). Kota Damansara vs Mutiara Damansara. Retrieved fromhttps://residentialpropertykl.com/compare/kota-damansara-vs-mutiara-damansara Sim, M. (2025, May 27). Neighbourhood Lens: Landed residential homes in Damansara Kim, PJ, still catching the eyes of homebuyers. EdgeProp. Retrieved fromhttps://www.edgeprop.my/content/1912645/neighbourhood-lens-landed-residential-homes-damansara-kim-pj-still-catching-eyes-homebuyers Wong, K. W. (2023, February 6). Rental Market: Bandar Sri Damansara benefiting from better infrastructure. The Edge Malaysia. Retrieved fromhttps://theedgemalaysia.com/node/653403 Yin Homes. (2026, March 17). KL Property Investment Comparison 2026: TTDI vs Bangsar, Mont Kiara & Damansara Heights - Yin Homes. Retrieved fromhttps://yinhomes.my/blog/ttdi-vs-bangsar-vs-mont-kiara-vs-damansara-heights

Continue Reading

Malaysia Subsale Home Prices Rise as KL Hits RM1 Million

Malaysia Subsale Home Prices Rise as KL Hits RM1 Million

Malaysia's secondary property market is heating up, and the latest numbers prove it. The average price of a subsale (resale) home in Malaysia rose 4.8% year-on-year to RM545,059 in the first quarter of 2026, according to Juwai IQI’s latest Residential Subsale Market Report. Even more striking? Kuala Lumpur has officially crossed the RM1 million barrier. The report is based on more than 230,000 residential subsale transactions recorded since 2018, giving a clearer picture of how Malaysia’s resale housing market is moving and where buyer demand remains strongest. The average price of a resale home in Malaysia climbed nearly five per cent over the past year, which reflects buyer confidence in the market. Kashif Ansari, Co-Founder and Group CEO of Juwai IQI Kuala Lumpur recorded the strongest price growth among the key markets highlighted in the report. In the capital, buyers paid 15% more on average for subsale homes in Q1 2026 compared to a year earlier. This pushed the average Kuala Lumpur subsale home price to RM1.02 million. Demand for resale houses was strongest in the first quarter. In Kuala Lumpur, the country's largest urban resale market, buyers paid 15 per cent more on average for subsale homes in the first quarter of 2026, compared to a year earlier. The average price for a subsale home in KL is now RM1.02 million. Kashif Ansari, co-founder and group CEO of Juwai IQI. Despite the stronger headline numbers, the report points to an encouraging trend for ordinary homebuyers. A large share of Malaysia’s subsale activity is still happening in the affordable and middle-market segments. Nearly one in four subsale transactions were for homes priced at RM250,000 or below, while roughly seven in ten transactions were for homes priced at RM500,000 or below. “So, a majority of purchases are made by entry-level and middle-market buyers. That’s good news,” said Kashif. This suggests that Malaysia’s subsale market is not being driven only by high-end purchases. Instead, demand remains broad-based, with many buyers still focused on practical and more affordable homes. If you're one of them, here's our step-by-step guide to buying a house in Malaysia The national average hides important regional differences. Here's how the key states performed: StateQ1 2026 TrendAverage Subsale PriceKuala Lumpur▲ Up 15%RM1.02 millionSelangor▬ Stable (largest market by volume)RM559,935Penang▼ Eased ~2%—Negeri Sembilan▼ Eased ~5%RM340,207Melaka—(now pricier than N. Sembilan) Selangor, the country's largest subsale market by transaction volume, stayed essentially flat year-on-year at RM559,935. Meanwhile, Penang and Negeri Sembilan saw modest easing of 2% and 5% respectively, consistent with the broader shift toward more entry-level price points. A notable change: Negeri Sembilan has overtaken Melaka as the most accessible market among these five states, with an average subsale price of just RM340,207. What This Means for Buyers and Investors? For homebuyers, the message is mixed but reassuring: while KL has crossed a symbolic threshold, affordable options remain widespread, especially in states like Negeri Sembilan and across the sub-RM500,000 band that dominates the market. For investors, the data points to where momentum lives, with KL commanding premium growth, while Selangor offers stability and emerging states offer accessible entry points. For those weighing the capital, here's why investors still choose KL. The subsale market remains a powerful indicator of real, transacted demand, because unlike new launches, these are prices buyers are actually paying today. Juwai IQI's Q1 2026 Residential Subsale Market Report was featured in Malay Mail. Juwai IQI is the world-renowned property company that provides insights on property, locally and globally. Click below to get more expert property insights from our blog! MORE INSIGHTS

Continue Reading

The Social Media Playbook Every Real Estate Agent Needs in 2026

The Social Media Playbook Every Real Estate Agent Needs in 2026

Picture this. An agent posts a beautiful listing with great photos, a fair price and a prime location, then waits. A few likes come in, maybe one “PM please” from someone who never replies. Meanwhile, another agent nearby, newer and with a smaller following, closes a deal from a 30-second video filmed on their phone during a viewing. Same market, same listings, but completely different results. If you have ever felt that gap, this story is for you. That gap is exactly why our marketing team built the IQI Social Media Playbook, a two-volume guide that turns “I should post more” into a clear system. This article shows what is inside, why it works and how it helps agents move from invisible to in-demand. TL;DR Social media is now essential for property agents in 2026. The IQI Social Media Playbook gives agents a clear system for what to post, where to post, how to generate leads, and how to stay consistent in just 21 days. Agents do not need a big following or a production team, only the right system and around three hours a week. Table of contentsWhat Is the IQI Social Media Playbook?Why Social Media Decides Who Wins in 2026Agents Who Turned Content Into ClientsInside the Playbook: The System That Closes the GapHow Agents Stack Up: With a System vs WithoutWhat Our Team Leads SayFAQs What Is the IQI Social Media Playbook? The IQI Social Media Playbook is a two-volume guide created by IQI’s marketing team to help property agents grow online with a clear system. It shows agents what to post on each platform, how to turn views into real conversations and how to stay consistent with a simple 21-day plan, all in around three hours a week. You do not need a big following or fancy equipment to start, just the right system to follow. VolumeWhat It CoversVol 1 — Build Your PresenceWhat to post on each platform, and how to pick your two.Vol 2 — Build Your PipelineTurning views into conversations, plus a 21-day plan. Why Social Media Decides Who Wins in 2026 Let’s be honest about the part nobody likes to admit. You know social media matters, so you try to post. A listing here, a market update there, maybe a motivational quote when you run out of ideas. Some posts get attention, most disappear, and after a while, you start wondering if you are just not the “social media type.” The truth is, it was never about being the social media type. It was about not having a system. Buyers today no longer wait for cold calls. They scroll Reels at midnight, watch property tours over lunch, and ask AI tools like ChatGPT and Gemini to shortlist agents before they ever pick up the phone. By the time a buyer messages you, they have already decided if they trust you. The good news? You no longer need a big ad budget or years of contacts. You just need to show up consistently. Visibility leads to consideration, and consideration leads to conversion. If you’re invisible at the top, nothing happens at the bottom. Jasmine Yap, Digital Marketing Manager, Juwai IQI If you want to strengthen your listing content first, our guide on how to write compelling property listings pairs well with everything in the Playbook. Agents Who Turned Content Into Clients The most convincing proof is not a statistic. It is the agents already living this, people who started exactly where you are now. Take Suthan Chelliah. He stopped treating his profile like a noticeboard for listings and started treating it like a relationship. Instead of just posting properties, I focus on sharing insights, success stories, and real experiences in the real estate journey. Suthan Chelliah, IQI agent (Elite team) Then there is Vincent Tai, who realised the goal was never to sell harder, but to help more. Social media is where we build trust with potential clients. It’s not just about selling houses, it’s about providing value and guiding people through every step of their journey. Vincent Tai, IQI agent (United team) Natasha Gideon proved you do not need a film crew or a perfect setup to begin. Don’t overthink production. Your audience values your knowledge more than high-end aesthetics. Natasha Gideon, IQI agent (Elite team) And Mark Lai learned that chasing viral numbers was the wrong target altogether. Focus on monetisation over views. Know who you’re making content for. Mark Lai, IQI agent (CS team) Different platforms, different styles, same lesson: when you show up as a real person with something useful to say, people trust you before you have even spoken. The only thing standing between you and that result is knowing how to do it on purpose, every week, without burning out. Inside the Playbook: The System That Closes the Gap Our marketing team kept seeing the same problem: talented agents were stuck, not because they lacked skill, but because they did not have a clear system to follow. So we built one. The Playbook is simple, practical and made for real agents, answering the three questions that stop most people from posting with confidence. “What do I even post?”Volume 1, Build Your Presence shows agents where to focus instead of trying to be everywhere. Pick one main platform and one supporting platform: Instagram for personal branding, Facebook for trust, TikTok for fast attention and YouTube for serious buyer research. “How does a post become a client?” Volume 2, Build Your Pipeline shows agents how to turn views into conversations. Instead of chasing leads, use simple prompts like “DM me ‘GUIDE’ for my first-time buyer checklist.” In the Playbook, one TikTok helped an agent book a RM480k unit in 19 days, with zero ad spend. “Where do I find the time?” The Playbook removes the “I do not have time” excuse with a simple system: create one main content piece, turn it into five posts, and follow the 21-Day Quick Start. Total time needed: around three hours a week. Once enquiries start coming in, use our lead conversion tips for property negotiators to turn interest into action. Your next lead may not come from a cold call. It could come from your next post. See how the IQI Social Media Playbook helps agents build that system. IQI Social Media Playbook How Agents Stack Up: With a System vs Without The difference between agents who struggle online and agents who grow rarely comes down to talent. It comes down to whether they are working from a system. Posting Without a SystemPosting With the PlaybookRandom posts, unpredictable resultsClear plan for what to post and whereSame content copied to every platformContent matched to each platform’s audiencePosts that get likes but no enquiriesPosts designed to start conversationsBurnout from trying to do everythingAround three hours a week, repurposed smartlyStarting alone with no feedbackTraining, tools and a community behind you What Our Team Leads Say Beyond the agents on the ground, the people who train them see the same pattern too. New agents who succeed are not always the loudest or most polished, but the ones who stay consistent and focus on helping people. Content isn’t marketing, it’s helping people. When you show up with answers instead of pitches, you become a trusted voice. Amir Asraf Lee, Senior Content Team Lead, Juwai IQI The Quick Start takes you from zero to a rhythm you can keep, one week at a time. WeekGoalFocusWeek 1Build awarenessShow who you are & who you helpWeek 2Build trustShare methods & real experienceWeek 3Drive enquiriesGently invite people to reach out One anchor post a week → repurposed into five. That is the whole secret to staying consistent without burning out. That is the mindset behind the Playbook. It also prepares agents for the future of search through the P.A.R. approach: Presence, Authority and Reputation, helping agents become the kind of trusted name that buyers and AI tools can recommend. Every agent starts unsure and unseen, but with the right system and company support, they can build visibility with confidence. FAQs Do I need a big following to get leads as a property agent? No. A brand new account can generate real leads without a large ad budget. Consistency, helpful content, and a clear way for people to reach out matter far more than follower count. Do I have to show my face on camera to succeed? No. You can start with carousels, market notes, and listing visuals without ever appearing on camera. Consistency matters more than format, and you can ease into video whenever you are ready. How much time does this actually take each week? Around three hours a week. Using the 1-to-5 Content Multiplier, you create one anchor piece and repurpose it into five posts, so you batch everything in a single session. Do I need to be on every social media platform? No, and trying to be is the fastest way to burn out. Pick one focused platform to go deep on and one complementary platform to repurpose to. The right combination is the one you will actually stick with. How do I get access to the full IQI Social Media Playbook? The complete two-volume Playbook is available to IQI agents. Join IQI as a REN to unlock both volumes, the full prompt bank, and the 21-day quick-start plan. Ready to grow your real estate career with IQI? Submit your details today and our team will guide you on how to start your journey as part of IQI’s global real estate network. [custom_blog_recruit_form] Continue Reading: Digital Marketing for Real Estate: Tips To Generate More Leads ChatGPT for Real Estate: Transforming the Way Agents Work Real Estate Agent Salary in Malaysia – How Much Do They Really Make? How Gen Z Can Benefit from a Property Agent Career Sources IQI Global. (2026). IQI Social Media Playbook 2026, Volume 1: Build Your Presence & Volume 2: Build Your Pipeline. Prepared by the Juwai IQI Digital Marketing Team. https://iqiglobal.com/playbook Aboulhosn, S. (2024). How to Craft an Effective Social Media Content Strategy. Sprout Social. https://sproutsocial.com/insights/social-media-content-strategy/ Buffer. (2024). Types of Social Media Content: 30+ Ideas for Your Next Post. https://buffer.com/resources/social-media-content-types/

Continue Reading

Got a question?

We're here to help you with any questions you may have. We'd love to talk about how we can help you.