The mortgage calculator is intended for reference only. Actual amount may vary.

Monthly Payment

Send me the mortgage calculator result

Embed this calculator on your website

Copy the code below and paste it into your site. Append ?theme=dark

or ?theme=light

to the src URL to match your site's theme.

<iframe src="https://iqiglobal.com/mortgage-calculator" width="100%" height="640" frameborder="0" title="IQI Mortgage Calculator" loading="lazy"></iframe>

Before you apply

Check Your Loan Eligibility First

Your Debt Service Ratio (DSR) determines whether a bank will approve your loan. Use our free DSR Calculator to see if you qualify before you apply.

New Launches

Latest Listings

Beach Pearl 3 Hotel

Diakopto Διακοπτό 250 03 Greece

Starting from € 205,000

Listed on July 4, 2025

Marousi - Athens

Marousi Μαρούσι Greece

Starting from € 310,000

Listed on July 4, 2025

Athens - Pallini

Pallini Παλλήνη Αττικής Greece

Starting from € 260,000

Listed on July 4, 2025

FAL 250

Palaio Faliro, Greece

Starting from € 800,000

Listed on July 3, 2025

Garden Polis I

Ακαδημία Πλάτωνος Athens 104 42 Greece

Starting from € 260,000

Listed on November 15, 2024

Garden Riviera I

Palaio Faliro Paleo Faliro, Greece

Starting from € 320,000

Listed on November 8, 2024

Learn

Tips and Guides

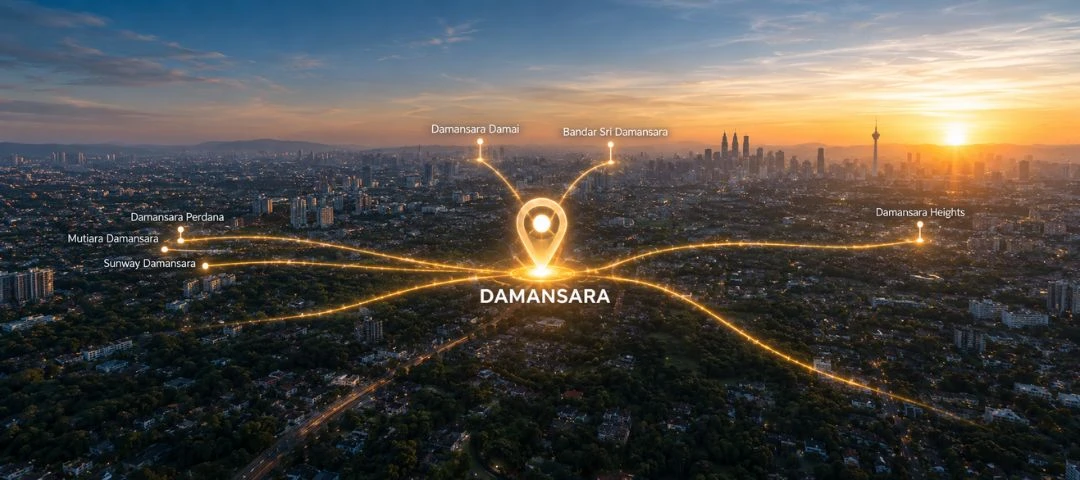

Damansara Rental Yield for Property Investment

Damansara Rental Yield for Property Investment

TL;DRDamansara rental yield is strongest when you buy the right property type in the right pocket, not just the most famous neighborhood. Based on various data, Damansara Perdana stands out for condo yield, while Sunway Damansara, Damansara Damai, and Bandar Sri Damansara show useful landed-house yield signals. Premium areas such as Damansara Heights and Mutiara Damansara can still be excellent long-term plays, but they are usually more about capital value than easy positive cash flow. Damansara sounds like one neat area, but for investors, it behaves more like a family WhatsApp group: same surname, very different personalities. One pocket offers a higher monthly rent, another protects long-term value, and another looks fancy but makes the yield do push-ups. This guide breaks down Damansara rental yield by area, property type, and tenant demand, so you do not buy with vibes alone. Key Takeaways Damansara Perdana rental yield is one of the clearest condo-yield opportunities, with implied yields of 3.85% and 6.33% for 1,001-1,500 sq ft units in its rental yield table. Sunway Damansara rental yield is a strong landed-house signal, reporting 5.04% for houses, although investors still need to compare the exact property condition, rentability, and entry price. Ara Damansara rental yield depends heavily on property type, with reports showing 2.05% for houses, while one expert places the gross yield for Ara Damansara condos at 4.5% to 5.5%. Kota Damansara rental demand is supported by MRT access, hospitals, schools, universities, malls, and commercial centers. Notably, 2,284 serviced apartments and condominium units are set to enter the market in 2026, which could pressure rents in the near term. Damansara Heights rental yield should be read carefully, as it varies by asset type. One reports 6% implied yield, while the luxury condo gross yield is at 3.0% to 4.0%, and a lower net yield for Damansara Heights by bedroom count. What You Should Know About Damansara Property1. What is the average Damansara rental yield in 2026?2. Which Damansara area has the best rental yield?3. How do you calculate rental yield for a Damansara property?4. Is a Damansara condo or a landed house better for rental income?5. Which Damansara areas have the strongest tenant demand?6. What risks should investors check before buying in Damansara?7. Is Damansara still a good place for property investment?8. Frequently Asked Questions (FAQs) Estimated reading time: 16 minutes 1. What is the average Damansara rental yield in 2026? Damansara rental yield can range from roughly 2% to above 6%, depending on neighborhood, property type, price per square foot, rent per square foot, and whether the yield is gross or net. The safest answer is this: Damansara is not one rental market. It is a cluster of different rental markets across Petaling Jaya and Kuala Lumpur. For example, iRumah reports Damansara Kim's house rental yield at 1.82%, while EdgeProp reports Damansara Kim’s implied rental yield at 2.23%. That difference already tells investors something important: different platforms may use different data pools, timeframes, and property samples. At the higher-yield end, EdgeProp reports Damansara Perdana at 3.85% implied yield, with a 6.33% rental yield for 1,001-1,500 sq ft units in its rental yield table. iRumah also reports Damansara Damai at 4.0% for houses and Sunway Damansara at 5.04% for houses. The practical lesson is simple: do not ask only, “What is the rental yield in Damansara?” Ask, “Which Damansara area, which property type, and at what purchase price?” a. Damansara rental yield comparison table Damansara areaproperty typeRental yield signalKey rental demand driverInvestor readingDamansara PerdanaCondominium/apartment3.85% implied yield; 6.33% for 1,001-1,500 sq ft unitsUrban lifestyle, studios, SOHO, proximity to Mutiara Damansara and PJStrongest condo yield signalSunway DamansaraHouses5.04%MRT, hospitals, universities, schools, Kota Damansara catchmentStrongly landed-house yield signalDamansara DamaiHouses4.0%MRT Damansara Damai, affordable housing baseAffordable entry with traffic caveatBandar Sri DamansaraHouses3.05%MRT, highways, mature township, schoolsStable practical demandDamansara JayaTerrace houses3.16% implied yield; 4.12% for 1,501-2,000 sq ft unitsMature PJ address, schools, Atria areaBetter yield than some mature landed pocketsAra DamansaraHouses/condos2.05% for houses; 4.5%-5.5% gross for condos (est.)LRT Ara Damansara, Subang, and PJ workforceBetter for condos than landed yieldMutiara DamansaraHouses2.72%MRT, malls, hospitals, and a premium lifestyleMore lifestyle and capital-value drivenDamansara KimTerrace houses1.82% to 2.23%Mature SS20 landed neighborhood, local amenitiesLower yield, mature landed appealDamansara HeightsDetached, semi-detached, terrace, land/luxury condos6% implied yield; 3.0%-4.0% luxury condo gross yieldPrestige, diplomats, legacy wealth, premium rentalsStrong address, yield depends heavily on asset typeSources: EdgeProp, iRumah, PropCashflow.my, Property Genie Data note: These figures are not all directly comparable because some refer to houses, some to condos, and some to broader implied yield. For a clean investment decision, compare similar units in the same building or on the same street, not just by area labels. 2. Which Damansara area has the best rental yield? Damansara Perdana has the strongest condo-yield signal, while Sunway Damansara has the strongest landed-house yield signal in the ingested data. For investors, that split matters because a condo rental and a landed house rental are not the same game. Damansara Perdana works well as a condo rental market because it has smaller units, studios, duplexes, and apartment rooms listed in the rental market, which can support more affordable monthly rent points. EdgeProp reports a median sale price of RM592 psf, a median rental price of RM1.58 psf, and an implied rental yield of 3.85% for Damansara Perdana. Its rental yield table also shows 1,001-1,500 sq ft units with an average monthly rent of RM2,600, an average price of RM497,397, and a rental yield of 6.33%. Sunway Damansara is different. iRumah reports a house rental yield of 5.04%, with house prices ranging from RM1.2 million to RM9.77 million. This makes it a strong landed-house signal, but the wide price range means investors must check whether the rent can really support the purchase price. Damansara Damai also deserves attention for rental income. iRumah reports a 4.0% rental yield for houses, with house market prices from RM760,000 to RM2.1 million. The advantage is affordability. The drawback is also stated in the source: peak-hour congestion and limited entry or exit access can affect daily living. a. Best Damansara area by investor goal Investor goalBest-fit areaWhy it fitsHighest condo yieldDamansara PerdanaStrong yield for 1,001-1,500 sq ft unitsStrong landed-house yieldSunway Damansara5.04% yield for housesAffordable landed-house yieldDamansara Damai4.0% yield and lower house entry rangeMature PJ stabilityBandar Sri DamansaraActive transactions and improved infrastructurePremium capital-value playMutiara Damansara, Damansara HeightsStronger lifestyle and prestige profile, but yield must be checked unit by unitTransit-linked condo strategyAra Damansara, Kota Damansara, Damansara PerdanaLRT, MRT, malls, and working populations support tenant demandSource: EdgeProp, iRumah, Brickz, The Edge Malaysia If you want a single clean answer, the best Damansara area for rental yield isn't a single neighborhood. It is the best match between yield, asset type, and tenant profile. For condo yield, start with Damansara Perdana. For landed yield, compare Sunway Damansara, Damansara Damai, and Bandar Sri Damansara carefully. 3. How do you calculate rental yield for a Damansara property? Gross rental yield is calculated by dividing annual rental income by property value, then multiplying by 100. It is the first fast check, but it is not the final investment answer. Use this formula: Gross rental yield = Annual rental income ÷ property value × 100 Let’s say a Damansara condo rents for RM2,600 per month and has an average price of RM497,397. Annual rental income is RM31,200. Using the gross yield formula, the rough result is about 6.3%, which is close to EdgeProp’s reported 6.33% rental yield for Damansara Perdana units sized 1,001-1,500 sq ft. But serious investors should also calculate net rental yield. PropCashflow defines net yield as annual rent minus operating costs, divided by purchase price, and includes costs such as maintenance fees, sinking fund, quit rent, assessment rates, rental income tax, vacancy allowance, and landlord insurance. Bamboo Routes also stresses that net yield matters because service charges, vacancy, repairs, leasing, and other costs reduce the actual return. Use this formula: Net rental yield = Annual rental income after costs ÷ property value × 100 Net rental yield is what remains after the property stops looking pretty on a spreadsheet and starts behaving like real property. Maintenance, repairs, vacancies, and furnishing costs all have a way of joining the party uninvited. 4. Is a Damansara condo or a landed house better for rental income? Damansara condo rental yields are usually easier to optimize than landed-house yields because condos often have lower entry prices, smaller unit sizes, and clearer tenant pools. Landed houses can still be valuable, but they often lean more toward long-term capital appreciation and family use. The clearest example is Damansara Perdana. EdgeProp reports a 6.33% yield for 1,001-1,500 sq ft units, indicating stronger income efficiency for selected condo or apartment stock. iRumah also shows Damansara Perdana rental listings for studios, duplexes, rooms, and shop-offices, suggesting a more varied rental market. For landed houses, results vary widely. iRumah reports rental yields of 2.05% for houses in Ara Damansara, 2.72% in Mutiara Damansara, 1.82% in Damansara Kim, and 3.05% in Bandar Sri Damansara. That does not mean landed homes are bad investments. It means that the Damansara landed house rental yield can be lower because buyers pay for land value, scarcity, neighborhood prestige, and family appeal. These qualities may support resale value, but they do not always push the monthly rental enough to create a high yield. a. Condo vs landed investment logic Property typeBetter forMain advantageMain riskCondo/apartmentRental yield and tenant flexibilityLower entry price and easier furnishing packageBuilding competition and service chargesServiced apartmentShort-term tenants and furnished rentalStrong rental appeal near malls or transitHigher maintenance and possible oversupplyLanded houseLong-term ownership and family tenantsLand value and capital appreciation potentialA higher purchase price can compress the yieldShop-officeCommercial rental incomeCan command higher rent in active commercial areasTenant quality and business-cycle risk For many first-time investors, a furnished condo rental near an MRT or LRT station is the easier starting point. Landed houses suit investors who can accept a lower yield while waiting for long-term capital appreciation. IQI Global can help investors compare both new launches and subsale property options, especially when the choice is not simply “buy where the yield looks highest.” Approach us now for more Damansara property! Find Damansara Property Now! 5. Which Damansara areas have the strongest tenant demand? Tenant demand is strongest where renters have daily reasons to stay: MRT and LRT stations, malls, hospitals, schools, universities, offices, highways, and lifestyle amenities. In Damansara, these points strongly point toward Kota Damansara, Ara Damansara, Damansara Perdana, Bandar Sri Damansara, and selected premium pockets. Kota Damansara has a strong rental story, supported by MRT access, malls, education, healthcare, and commercial centers. Kota Damansara is served by Surian MRT, Kota Damansara MRT, and Kampung Selamat MRT, and has amenities such as The Strand Mall, Sunway Nexis Mall, Sunway Giza Mall, and Tropicana Gardens Mall. According to The Edge Malaysia, working adults and students from nearby universities drive demand for high-rise residential properties. Ara Damansara is another strong area for tenant demand, especially for condos near transit. LRT Ara Damansara, LRT Kelana Jaya, and LRT Lembah Subang are nearby transit stations. PropCashflow places the Ara Damansara condo gross yield at 4.5% to 5.5%, supported by the LRT Kelana Jaya Line, the Subang and PJ workforce, proximity to Subang Airport, and Evolve Concept Mall. Bandar Sri Damansara has a practical occupancy rate story. The Edge Malaysia reports that condominium units and apartments there had 80% to 90% occupancy, while offices, shophouses, and retail shops at Ativo Plaza and 8trium had 70% to 90% occupancy Brickz also reports 215 residential transactions in Bandar Sri Damansara between May 2025 and April 2026, with a median PSF of RM507 and a median property price of RM480,000. Damansara Heights and Mutiara Damansara have different rental demand profiles. They are not mainly affordability plays. Mutiara Damansara is supported by malls, MRT, and premium township planning, while Damansara Heights attracts legacy wealth, diplomats, and premium renters according to Property Genie’s luxury condo comparison. 6. What risks should investors check before buying in Damansara? Investment property decisions in Malaysia should never rely solely on the headline rental yield. In Damansara, investors must check the property type, source of funds, vacancy risk, maintenance costs, new supply, traffic, and whether the quoted yield is gross or net. First, check the new supply risk. Kota Damansara has a strong demand, but The Edge Malaysia reports that in 2024, three ongoing projects will add 2,284 serviced apartments and condominium units over the next two years. More units can give tenants more choices, which may pressure rental growth if supply rises faster than demand. Second, check gross rental yield against net rental yield. A few experts both make the same practical point: gross yield is only the first screen, while net yield must deduct real operating costs. If your condo looks good at 5% gross but has high service charges, long vacancy periods, and heavy furnishing costs, the real return can shrink quickly. Third, check whether the property is leasehold or freehold. For example, Sunway Damansara and Damansara Perdana are leasehold, while Mutiara Damansara is freehold. Tenure alone does not decide investment quality, but it affects buyer perception, financing comfort, and long-term resale confidence. Fourth, check traffic and access. Traffic congestion challenges in Ara Damansara and Damansara Damai, with Damansara Damai facing peak-hour issues because of limited entry and exit access. A renter may love cheap rent, but not if the daily commute feels like a boss fight. Finally, check the property value versus the rental income. Newprojek reports Mutiara Damansara’s median price at RM1.50 million and median PSF at RM868 based on 67 verified transactions from October 2021 to February 2026. iRumah reports Mutiara Damansara house rental yield at 2.72%. That combination suggests investors should treat Mutiara Damansara more as a premium lifestyle or capital-value market than a pure cash-flow play. IQI Global is useful here because investors often need help comparing not just listing price, but also rentability, furnishing strategy, tenant profile, and resale appeal. We can help you with that! Let Us Help You! 7. Is Damansara still a good place for property investment? Damansara property investment remains attractive, but the best strategy is to choose based on the investor's goals rather than chasing a single “best” area. For rental yield, start with Damansara Perdana, Sunway Damansara, Damansara Damai, and Bandar Sri Damansara. For tenant depth, focus on Kota Damansara, Ara Damansara, and Damansara Perdana. For long-term capital preservation, study Mutiara Damansara and Damansara Heights. If you want positive cash flow, you need to be strict. Compare the monthly rent, maintenance fees, vacancy risk, and loan payments before buying. Various pieces of information support a clear pattern: smaller or mid-sized units near transit and amenities are easier to shape into rental investments, while premium landed homes may require a longer holding horizon. If you want capital appreciation, mature and premium pockets can still make sense. Mutiara Damansara shows a median price of RM1.50 million and a +6.4% increase since 2021 on Newprojek’s transaction page. Damansara Heights is repeatedly framed as a prestige and legacy-wealth area by EdgeProp and Property Genie. If you want a balanced property investment, the sweet spot is a property with an acceptable rental yield, strong tenant demand, and realistic resale value. In layman's terms, buy something people actually want to live in, at a price that still makes the rent work. IQI Global can help buyers and investors explore opportunities in Damansara, compare rental demand across neighborhoods, and shortlist properties that align with both income and long-term value goals. Explore Damansara Property Damansara rental yield is not about picking the fanciest name on the map. It is about matching the right property type to the right tenant pool at the right price. Damansara Perdana looks strongest for sourced condo yield, while Sunway Damansara and Damansara Damai show useful landed-house signals. For a safer investment, compare yield, demand, costs, and resale value together. 8. Frequently Asked Questions (FAQs) a. What is the rental yield in Damansara? Damansara rental yield varies by area and property type. The ingested sources show lower house yields in mature landed areas, such as Damansara Kim, while condo-focused areas, such as Damansara Perdana, show stronger sourced rental yield signals. b. Which Damansara area has the best rental yield? Damansara Perdana has the strongest condo-yield signal, with an implied yield of 3.85% and 6.33% for 1,001-1,500 sq ft units. For houses, Sunway Damansara shows a strong sourced yield at 5.04%. c. How do I calculate rental yield for a Damansara property? Rental yield is calculated by dividing annual rental income by property value, then multiplying by 100. For net yield, deduct costs such as maintenance, vacancy, tax, insurance, and repairs before dividing by the property value. d. Is Ara Damansara better than Damansara Perdana for rental income? Ara Damansara is better for LRT-linked professional demand, while Damansara Perdana has a clearer condo-yield signal. Ara Damansara house yields at 2.05%, while Damansara Perdana’s implied yield is at 3.85%, and the selected unit yields at 6.33%. e. Should I buy a condo or a landed house in Damansara for rental income? Condo rentals are usually easier to rent out because entry prices are often lower and tenant pools are broader near transit, malls, and offices. Landed homes in Damansara can still be strong long-term assets, but high property value can reduce yield efficiency. f. Is Damansara Heights good for rental yield? Damansara Heights rental yield depends heavily on asset type. 6% implied yield, but a luxury condo gross yield at 3.0% to 4.0%, and a lower net yield for Damansara Heights by bedroom count. g. What is a good rental yield for property investment in Malaysia? Good rental yield depends on risk, costs and location, not just percentage. PropCashflow ranks many stronger Malaysian urban yield areas around 4.5% to 7.5% gross, while Bamboo Routes stresses that net yield is more important after costs and vacancy. IQI Global can help you compare properties in Damansara based on yield, tenant demand, and long-term value. Explore your next investment with our team today. [custom_blog_form] Continue Reading: Property Overhang vs Unsold Property in Malaysia: What Buyers Must Know What is Debt-To-Service Ratio (DSR) in Malaysia & How It Affects Your Home Loan What Is eSPA? Malaysia’s New Initiative to Help Homebuyers Buy Faster Sources and References Bamboo Routes. (2026, January 13). What rental yield can you expect in Malaysia? (2026). Retrieved fromhttps://bambooroutes.com/blogs/news/malaysia-rental-yields Brickz. (n.d.). BANDAR SRI DAMANSARA, SELANGOR - RESIDENTIAL. Retrieved fromhttps://www.brickz.my/transactions/residential/selangor/bandar-sri-damansara/ Chai, Y. H. (2023, April 13). Rental Market: Bandar Utama terraced houses enjoy strong rental demand. The Edge Malaysia. Retrieved fromhttps://theedgemalaysia.com/node/662066 Chai, Y. H. (2024, June 26). Rental Market: Kota Damansara’s rental market buoyed by strategic location, good amenities. The Edge Malaysia. Retrieved fromhttps://theedgemalaysia.com/node/715384 EdgeProp. (n.d.). Ara Damansara. Retrieved fromhttps://www.edgeprop.my/area-outlook/selangor/ara-damansara EdgeProp. (n.d.). Damansara Heights (Bukit Damansara), Damansara Heights Insights. Retrieved fromhttps://www.edgeprop.my/project/damansara-heights-bukit-damansara--16828 EdgeProp. (n.d.). Damansara Jaya, Petaling Jaya Insights. Retrieved fromhttps://www.edgeprop.my/project/damansara-jaya-14418 EdgeProp. (n.d.). Damansara Kim, Damansara Insights. Retrieved fromhttps://www.edgeprop.my/project/damansara-kim-9391 EdgeProp. (n.d.). Damansara Perdana, Petaling Jaya Insights. Retrieved fromhttps://www.edgeprop.my/condo/damansara-perdana-30168 Hartamas. (2026, March 30). Arra Residences Ara Damansara: An Honest 5-Question Review (2025) - Hartamas Real Estate. Retrieved fromhttps://hartamas.com/arra-residences-ara-damansara-an-honest-5-question-review-2025/ iHome.my. (2026, June 19). Buying or Renting in Damansara 2026: Kota Damansara, Mutiara, TTDI Guide. Retrieved fromhttps://ihome.my/areas/damansara-property-guide/ iRumah. (n.d.). Ara Damansara, Petaling Jaya. Retrieved fromhttps://irumah.co/petaling-jaya/ara-damansara iRumah. (n.d.). Bandar Sri Damansara, Petaling Jaya. Retrieved fromhttps://irumah.co/petaling-jaya/bandar-sri-damansara iRumah. (n.d.). Damansara Damai, Petaling Jaya. Retrieved fromhttps://irumah.co/petaling-jaya/damansara-damai iRumah. (n.d.). Damansara Jaya, Petaling Jaya. Retrieved fromhttps://irumah.co/petaling-jaya/damansara-jaya iRumah. (n.d.). Damansara Kim, Damansara Utama. Retrieved fromhttps://irumah.co/damansara-utama/damansara-kim iRumah. (n.d.). Damansara Perdana, Petaling Jaya. Retrieved fromhttps://irumah.co/petaling-jaya/damansara-perdana iRumah. (n.d.). Damansara Utama, Petaling Jaya. Retrieved fromhttps://irumah.co/petaling-jaya/damansara-utama iRumah. (n.d.). Mutiara Damansara, Petaling Jaya. Retrieved fromhttps://irumah.co/petaling-jaya/mutiara-damansara iRumah. (n.d.). Sunway Damansara, Kota Damansara. Retrieved fromhttps://irumah.co/kota-damansara/sunway-damansara Lee, R. (2026, March 18). Market Pulse: Steady growth keeps Damansara Uptown buzzing. The Edge Malaysia. Retrieved fromhttps://theedgemalaysia.com/node/795321 Newprojek. (2026, January 1). Best Property Investment in Petaling Jaya 2026. Retrieved fromhttps://newprojek.com/guides/best-property-investment-petaling-jaya Newprojek. (n.d.). MUTIARA DAMANSARA Property Value & Price History. Retrieved fromhttps://newprojek.com/property-transaction/mutiara-damansara PropCashflow.my. (2026, February 23). Best Rental Yield Areas in Malaysia 2026: Top 15 Ranked. Retrieved fromhttps://propcashflow.my/blog/best-rental-yield-areas-malaysia-2026-ranked/ Property Genie. (n.d.). Luxury Condo Kuala Lumpur 2026: KLCC, Mont Kiara, Bangsar, TTDI & Damansara Heights Compared. Retrieved fromhttps://www.propertygenie.com.my/insider-guide/luxury-condo-kuala-lumpur-2026-klcc-mont-kiara-bangsar-ttdi-damansara-heights-compared-P5aEk63pS4C4LHerKrVZVh Residential Property KL. (n.d.). Kota Damansara vs Mutiara Damansara. Retrieved fromhttps://residentialpropertykl.com/compare/kota-damansara-vs-mutiara-damansara Sim, M. (2025, May 27). Neighbourhood Lens: Landed residential homes in Damansara Kim, PJ, still catching the eyes of homebuyers. EdgeProp. Retrieved fromhttps://www.edgeprop.my/content/1912645/neighbourhood-lens-landed-residential-homes-damansara-kim-pj-still-catching-eyes-homebuyers Wong, K. W. (2023, February 6). Rental Market: Bandar Sri Damansara benefiting from better infrastructure. The Edge Malaysia. Retrieved fromhttps://theedgemalaysia.com/node/653403 Yin Homes. (2026, March 17). KL Property Investment Comparison 2026: TTDI vs Bangsar, Mont Kiara & Damansara Heights - Yin Homes. Retrieved fromhttps://yinhomes.my/blog/ttdi-vs-bangsar-vs-mont-kiara-vs-damansara-heights

Continue Reading

Malaysia Subsale Home Prices Rise as KL Hits RM1 Million

Malaysia Subsale Home Prices Rise as KL Hits RM1 Million

Malaysia's secondary property market is heating up, and the latest numbers prove it. The average price of a subsale (resale) home in Malaysia rose 4.8% year-on-year to RM545,059 in the first quarter of 2026, according to Juwai IQI’s latest Residential Subsale Market Report. Even more striking? Kuala Lumpur has officially crossed the RM1 million barrier. The report is based on more than 230,000 residential subsale transactions recorded since 2018, giving a clearer picture of how Malaysia’s resale housing market is moving and where buyer demand remains strongest. The average price of a resale home in Malaysia climbed nearly five per cent over the past year, which reflects buyer confidence in the market. Kashif Ansari, Co-Founder and Group CEO of Juwai IQI Kuala Lumpur recorded the strongest price growth among the key markets highlighted in the report. In the capital, buyers paid 15% more on average for subsale homes in Q1 2026 compared to a year earlier. This pushed the average Kuala Lumpur subsale home price to RM1.02 million. Demand for resale houses was strongest in the first quarter. In Kuala Lumpur, the country's largest urban resale market, buyers paid 15 per cent more on average for subsale homes in the first quarter of 2026, compared to a year earlier. The average price for a subsale home in KL is now RM1.02 million. Kashif Ansari, co-founder and group CEO of Juwai IQI. Despite the stronger headline numbers, the report points to an encouraging trend for ordinary homebuyers. A large share of Malaysia’s subsale activity is still happening in the affordable and middle-market segments. Nearly one in four subsale transactions were for homes priced at RM250,000 or below, while roughly seven in ten transactions were for homes priced at RM500,000 or below. “So, a majority of purchases are made by entry-level and middle-market buyers. That’s good news,” said Kashif. This suggests that Malaysia’s subsale market is not being driven only by high-end purchases. Instead, demand remains broad-based, with many buyers still focused on practical and more affordable homes. If you're one of them, here's our step-by-step guide to buying a house in Malaysia The national average hides important regional differences. Here's how the key states performed: StateQ1 2026 TrendAverage Subsale PriceKuala Lumpur▲ Up 15%RM1.02 millionSelangor▬ Stable (largest market by volume)RM559,935Penang▼ Eased ~2%—Negeri Sembilan▼ Eased ~5%RM340,207Melaka—(now pricier than N. Sembilan) Selangor, the country's largest subsale market by transaction volume, stayed essentially flat year-on-year at RM559,935. Meanwhile, Penang and Negeri Sembilan saw modest easing of 2% and 5% respectively, consistent with the broader shift toward more entry-level price points. A notable change: Negeri Sembilan has overtaken Melaka as the most accessible market among these five states, with an average subsale price of just RM340,207. What This Means for Buyers and Investors? For homebuyers, the message is mixed but reassuring: while KL has crossed a symbolic threshold, affordable options remain widespread, especially in states like Negeri Sembilan and across the sub-RM500,000 band that dominates the market. For investors, the data points to where momentum lives, with KL commanding premium growth, while Selangor offers stability and emerging states offer accessible entry points. For those weighing the capital, here's why investors still choose KL. The subsale market remains a powerful indicator of real, transacted demand, because unlike new launches, these are prices buyers are actually paying today. Juwai IQI's Q1 2026 Residential Subsale Market Report was featured in Malay Mail. Juwai IQI is the world-renowned property company that provides insights on property, locally and globally. Click below to get more expert property insights from our blog! MORE INSIGHTS

Continue Reading

The Social Media Playbook Every Real Estate Agent Needs in 2026

The Social Media Playbook Every Real Estate Agent Needs in 2026

Picture this. An agent posts a beautiful listing with great photos, a fair price and a prime location, then waits. A few likes come in, maybe one “PM please” from someone who never replies. Meanwhile, another agent nearby, newer and with a smaller following, closes a deal from a 30-second video filmed on their phone during a viewing. Same market, same listings, but completely different results. If you have ever felt that gap, this story is for you. That gap is exactly why our marketing team built the IQI Social Media Playbook, a two-volume guide that turns “I should post more” into a clear system. This article shows what is inside, why it works and how it helps agents move from invisible to in-demand. TL;DR Social media is now essential for property agents in 2026. The IQI Social Media Playbook gives agents a clear system for what to post, where to post, how to generate leads, and how to stay consistent in just 21 days. Agents do not need a big following or a production team, only the right system and around three hours a week. Table of contentsWhat Is the IQI Social Media Playbook?Why Social Media Decides Who Wins in 2026Agents Who Turned Content Into ClientsInside the Playbook: The System That Closes the GapHow Agents Stack Up: With a System vs WithoutWhat Our Team Leads SayFAQs What Is the IQI Social Media Playbook? The IQI Social Media Playbook is a two-volume guide created by IQI’s marketing team to help property agents grow online with a clear system. It shows agents what to post on each platform, how to turn views into real conversations and how to stay consistent with a simple 21-day plan, all in around three hours a week. You do not need a big following or fancy equipment to start, just the right system to follow. VolumeWhat It CoversVol 1 — Build Your PresenceWhat to post on each platform, and how to pick your two.Vol 2 — Build Your PipelineTurning views into conversations, plus a 21-day plan. Why Social Media Decides Who Wins in 2026 Let’s be honest about the part nobody likes to admit. You know social media matters, so you try to post. A listing here, a market update there, maybe a motivational quote when you run out of ideas. Some posts get attention, most disappear, and after a while, you start wondering if you are just not the “social media type.” The truth is, it was never about being the social media type. It was about not having a system. Buyers today no longer wait for cold calls. They scroll Reels at midnight, watch property tours over lunch, and ask AI tools like ChatGPT and Gemini to shortlist agents before they ever pick up the phone. By the time a buyer messages you, they have already decided if they trust you. The good news? You no longer need a big ad budget or years of contacts. You just need to show up consistently. Visibility leads to consideration, and consideration leads to conversion. If you’re invisible at the top, nothing happens at the bottom. Jasmine Yap, Digital Marketing Manager, Juwai IQI If you want to strengthen your listing content first, our guide on how to write compelling property listings pairs well with everything in the Playbook. Agents Who Turned Content Into Clients The most convincing proof is not a statistic. It is the agents already living this, people who started exactly where you are now. Take Suthan Chelliah. He stopped treating his profile like a noticeboard for listings and started treating it like a relationship. Instead of just posting properties, I focus on sharing insights, success stories, and real experiences in the real estate journey. Suthan Chelliah, IQI agent (Elite team) Then there is Vincent Tai, who realised the goal was never to sell harder, but to help more. Social media is where we build trust with potential clients. It’s not just about selling houses, it’s about providing value and guiding people through every step of their journey. Vincent Tai, IQI agent (United team) Natasha Gideon proved you do not need a film crew or a perfect setup to begin. Don’t overthink production. Your audience values your knowledge more than high-end aesthetics. Natasha Gideon, IQI agent (Elite team) And Mark Lai learned that chasing viral numbers was the wrong target altogether. Focus on monetisation over views. Know who you’re making content for. Mark Lai, IQI agent (CS team) Different platforms, different styles, same lesson: when you show up as a real person with something useful to say, people trust you before you have even spoken. The only thing standing between you and that result is knowing how to do it on purpose, every week, without burning out. Inside the Playbook: The System That Closes the Gap Our marketing team kept seeing the same problem: talented agents were stuck, not because they lacked skill, but because they did not have a clear system to follow. So we built one. The Playbook is simple, practical and made for real agents, answering the three questions that stop most people from posting with confidence. “What do I even post?”Volume 1, Build Your Presence shows agents where to focus instead of trying to be everywhere. Pick one main platform and one supporting platform: Instagram for personal branding, Facebook for trust, TikTok for fast attention and YouTube for serious buyer research. “How does a post become a client?” Volume 2, Build Your Pipeline shows agents how to turn views into conversations. Instead of chasing leads, use simple prompts like “DM me ‘GUIDE’ for my first-time buyer checklist.” In the Playbook, one TikTok helped an agent book a RM480k unit in 19 days, with zero ad spend. “Where do I find the time?” The Playbook removes the “I do not have time” excuse with a simple system: create one main content piece, turn it into five posts, and follow the 21-Day Quick Start. Total time needed: around three hours a week. Once enquiries start coming in, use our lead conversion tips for property negotiators to turn interest into action. Your next lead may not come from a cold call. It could come from your next post. See how the IQI Social Media Playbook helps agents build that system. IQI Social Media Playbook How Agents Stack Up: With a System vs Without The difference between agents who struggle online and agents who grow rarely comes down to talent. It comes down to whether they are working from a system. Posting Without a SystemPosting With the PlaybookRandom posts, unpredictable resultsClear plan for what to post and whereSame content copied to every platformContent matched to each platform’s audiencePosts that get likes but no enquiriesPosts designed to start conversationsBurnout from trying to do everythingAround three hours a week, repurposed smartlyStarting alone with no feedbackTraining, tools and a community behind you What Our Team Leads Say Beyond the agents on the ground, the people who train them see the same pattern too. New agents who succeed are not always the loudest or most polished, but the ones who stay consistent and focus on helping people. Content isn’t marketing, it’s helping people. When you show up with answers instead of pitches, you become a trusted voice. Amir Asraf Lee, Senior Content Team Lead, Juwai IQI The Quick Start takes you from zero to a rhythm you can keep, one week at a time. WeekGoalFocusWeek 1Build awarenessShow who you are & who you helpWeek 2Build trustShare methods & real experienceWeek 3Drive enquiriesGently invite people to reach out One anchor post a week → repurposed into five. That is the whole secret to staying consistent without burning out. That is the mindset behind the Playbook. It also prepares agents for the future of search through the P.A.R. approach: Presence, Authority and Reputation, helping agents become the kind of trusted name that buyers and AI tools can recommend. Every agent starts unsure and unseen, but with the right system and company support, they can build visibility with confidence. FAQs Do I need a big following to get leads as a property agent? No. A brand new account can generate real leads without a large ad budget. Consistency, helpful content, and a clear way for people to reach out matter far more than follower count. Do I have to show my face on camera to succeed? No. You can start with carousels, market notes, and listing visuals without ever appearing on camera. Consistency matters more than format, and you can ease into video whenever you are ready. How much time does this actually take each week? Around three hours a week. Using the 1-to-5 Content Multiplier, you create one anchor piece and repurpose it into five posts, so you batch everything in a single session. Do I need to be on every social media platform? No, and trying to be is the fastest way to burn out. Pick one focused platform to go deep on and one complementary platform to repurpose to. The right combination is the one you will actually stick with. How do I get access to the full IQI Social Media Playbook? The complete two-volume Playbook is available to IQI agents. Join IQI as a REN to unlock both volumes, the full prompt bank, and the 21-day quick-start plan. Ready to grow your real estate career with IQI? Submit your details today and our team will guide you on how to start your journey as part of IQI’s global real estate network. [custom_blog_recruit_form] Continue Reading: Digital Marketing for Real Estate: Tips To Generate More Leads ChatGPT for Real Estate: Transforming the Way Agents Work Real Estate Agent Salary in Malaysia – How Much Do They Really Make? How Gen Z Can Benefit from a Property Agent Career Sources IQI Global. (2026). IQI Social Media Playbook 2026, Volume 1: Build Your Presence & Volume 2: Build Your Pipeline. Prepared by the Juwai IQI Digital Marketing Team. https://iqiglobal.com/playbook Aboulhosn, S. (2024). How to Craft an Effective Social Media Content Strategy. Sprout Social. https://sproutsocial.com/insights/social-media-content-strategy/ Buffer. (2024). Types of Social Media Content: 30+ Ideas for Your Next Post. https://buffer.com/resources/social-media-content-types/

Continue Reading

Nobody Told Me My RM500k House Would Actually Cost RM700k

Nobody Told Me My RM500k House Would Actually Cost RM700k

TL;DR (the part you screenshot before scrolling)1) A RM500,000 house in Malaysia realistically costs RM650,000 to RM700,000+ once you add upfront fees, renovation, and furnishing.2) Before you move in, you typically need RM60,000 to RM90,000 in cash for the down payment, legal fees, and stamp duty.3) Good news for first-timers: under Budget 2026, Malaysian citizens buying their first home priced up to RM500,000 get 100% stamp duty exemption on the transfer and loan agreement until 31 Dec 2027.4) The monster nobody talks about is loan interest: borrowing RM450,000 at around 4% over 30 to 35 years adds roughly RM320,000 to RM390,000 in interest.5) The smarter question is not "can I afford the loan?" It is "can I afford everything after the loan?" And honestly? This is exactly why a lot of Malaysians end up regretting buying too early. Let us tell you a story. Meet Amir. He is 29, earns RM5,000 a month, and has saved up a respectable RM60,000. One day he finds a house he loves, priced at RM500,000. He looks at his savings, looks at the price tag, and thinks, "Yay! Dah boleh beli!" Then reality arrived. And reality, as many of you already know, does not knock politely. Here is the uncomfortable truth nobody puts on the showroom banner: in Malaysia, a RM500,000 house is almost never a RM500,000 decision. So before you sign anything, let us walk through the real math together, the way a good friend (or a slightly blunt property agent) would. Table of contentsSo how much does a RM500k house really cost?Step 1: The upfront costs before you even move in"Wait, don't first-time buyers skip stamp duty?"Step 2: Renovation and furnishing, the silent budget killersStep 3: Adding it all up (deep breath)"You forgot the interest" (yes, let us fix that)Find out what you can actually borrowWhy some people sell so soon after buyingAre houses just overpriced now? A fair questionThe one question to ask before you buy anythingSticker price vs real cost: a quick comparisonA bit of market context (so this isn't just our opinion)A quick word from the people who do this dailyFrequently Asked QuestionsBuying soon? Get your real numbers first. So how much does a RM500k house really cost? Short answer: a RM500,000 house in Malaysia usually ends up costing around RM650,000 to RM700,000 once you include upfront costs (down payment, legal fees, and stamp duty), renovation, and furnishing. On top of that, you should have roughly RM60,000 to RM90,000 in ready cash before collecting your keys. And if you count the interest over a 30 to 35 year loan, the total amount you actually repay can climb close to RM900,000 or more. The sticker price is the deposit on the truth, not the full story. Now let us break that down, step by step, because this is where most people get surprised. Step 1: The upfront costs before you even move in Let us do some simple Malaysian math on Amir's RM500,000 house. Down payment (10%): RM50,000 Legal fees + stamp duty: roughly RM10,000 to RM18,000 Loan agreement legal fees: already included in the figure above, but worth flagging separately because banks bill it on its own So before Amir even smells fresh paint, he is already looking at around RM60,000 to RM70,000 gone. Just like that. His RM60,000 savings? Basically used up on the deposit and fees alone. "But where do these legal fees and stamp duty numbers come from?" Fair question. Here is the actual 2026 breakdown so you are not just trusting vibes. Cost itemHow it is calculated (2026)Estimate on RM500k house / RM450k loanMOT stamp duty (transfer)1% on first RM100k, 2% on next RM400k~RM9,000Loan agreement stamp dutyFlat 0.5% of the loan amount~RM2,250SPA legal fee1.25% on first RM500k (SRO 2023)~RM6,250Loan legal fee1.25% on first RM500k of the loan~RM5,625Disbursements + searchesFixed per document~RM1,000 to RM2,000 Add those up and a non first-time buyer can easily cross RM20,000 in fees and duty on top of the deposit. That is not a typo. That is just Malaysia saying hello. "Wait, don't first-time buyers skip stamp duty?" Yes! And we love that you asked, because this is the bit that genuinely saves you money. Under Budget 2026, if you are a Malaysian citizen buying your first residential property priced up to RM500,000, you get a 100% stamp duty exemption on both the Memorandum of Transfer and the loan agreement. This exemption applies to Sale and Purchase Agreements signed between 1 January 2026 and 31 December 2027. In plain terms, that is roughly RM11,250 saved for someone like Amir. His upfront fees suddenly look a lot friendlier, mostly just legal fees and disbursements. Quick reality check: the exemption covers stamp duty, not legal fees. Lawyers still need to be paid (they have bills too). And the exemption is only for citizens buying their first home at or below RM500,000. Cross that price by even one ringgit and the rules change. So if you are hovering near the line, the price you negotiate matters more than you think. Step 2: Renovation and furnishing, the silent budget killers Okay, deposit paid, fees settled. Now comes the part everyone underestimates. And we mean everyone. Here is the list that quietly empties bank accounts across the country: Renovation Kitchen Wardrobe Lighting Fans Aircond Grilles Curtains And the famous "many more" For many Malaysians, this is where RM30,000 to RM100,000+ can disappear faster than kuih at a morning meeting. A built-in kitchen alone can run five figures. Aircond for three rooms, another chunk. Grilles for safety, because we all know that one auntie story. And then, congratulations, you finally get your keys! Time to relax, right? Not quite. Now you pay for the move-in installations: Unifi (because working from home without wifi is just sitting in a room) Indah Water connection Tenaga Nasional deposit and setup Bed, sofa, TV, the actual furniture that makes a house a home Suddenly another RM10,000 to RM30,000 is gone. You are now living in a beautiful home and quietly hugging a piggy bank. Step 3: Adding it all up (deep breath) Here is where it gets a little scary. That RM500k house can easily become: ItemAmountHouse priceRM500,000Upfront costs (deposit, fees, duty)RM70,000RenovationRM80,000FurnishingRM20,000Total (and we are being conservative)RM670,000 And yes, that figure is on the polite side. Push the renovation or buy in a pricier area and you are knocking on RM700,000 without trying. A RM500k house that quietly became a RM700k commitment. Nobody warned Amir. We are warning you. "You forgot the interest" (yes, let us fix that) One of you actually caught this on our socials, and it was a sharp catch: "You forget to factor in progressive interest on the upfront cost."- a very switched-on commenter, and they are right So let us add the part that hurts the most over time. When Amir borrows RM450,000 (after his 10% down payment), he does not just repay RM450,000. He repays that plus interest, spread across 30 to 35 years. For context, Bank Negara's Overnight Policy Rate has sat at 2.75% since July 2025, and effective home loan rates in 2026 generally land somewhere around 3.8% to 4.6%. Using roughly 4% as an example: Over 30 years, total interest is around RM320,000. Over 35 years, total interest climbs to around RM390,000. Read that again. The interest alone can almost equal the price of the house. So that "RM500k house" might cost you closer to RM900,000 to RM1 million across the full life of the loan. (Figures are illustrative and depend on your bank, rate, and tenure, but the shape of the lesson does not change.) Small move, big savings: even a 0.5% difference in your loan rate can mean tens of thousands of ringgit over the tenure. Comparing banks for 30 minutes is genuinely one of the best-paid half hours of your life. Find out what you can actually borrow All this math leads to one very practical question: how much will a bank actually lend you? Your loan eligibility is not just about the price tag. It depends on your income, your existing commitments, and your debt service ratio. Two people eyeing the same RM500,000 house can qualify for very different loan amounts. So before you start viewing homes and emotionally moving in, take 60 seconds to find your real number. Try the IQI Home Loan Eligibility Calculator below. It gives you a quick, no-strings estimate of what you may qualify for, so you can shop with confidence instead of guesswork. Want to crunch the other numbers too, like your monthly instalment, stamp duty, or overall affordability? You will find the full set of free tools on the IQI Calculators page. Bookmark it. Your future self (and your wallet) will thank you. Why some people sell so soon after buying This is the real reason behind a pattern we see often. Some people sell their home not long after buying it. And usually it is not because they hate the house. It is not because the location is bad. It is because they underestimated the real cost of ownership. The monthly instalment? That part was manageable. They budgeted for it. It was everything else that wasn't. The renovation that ballooned. The furniture on instalment. The aircond servicing, the quit rent, the maintenance fees, the surprise plumbing. Life after the loan turned out to be more expensive than the loan itself. One commenter put it perfectly in pure Malaysian wisdom: "Wajib buat kira-kira sebelum beli rumah. Bukan ikut tekak, tapi poket."Translation: You must do the calculations before buying a house. Do not follow your cravings, follow your wallet. Frame that and hang it on your future wall. Are houses just overpriced now? A fair question Another reader said what plenty of people are thinking: "It's because houses are overpriced now."- and this deserves an honest answer, not a sales pitch It is a fair point. Affordability has genuinely tightened. Many projects launched during the low-rate years of 2020 to 2022 still carry asking prices anchored to that era, while household debt in Malaysia sits in the trillions. When borrowing capacity drops, some of those prices start to look stretched. But here is the thing. "Overpriced" is not one number for the whole country. It depends heavily on the area, the property type, the tenure, and whether you are buying a home to live in or an asset to rent out. A unit that looks overpriced in one township can be a steal two stops down the MRT line. Which is exactly why knowing your real all-in cost matters more in an expensive market, not less. You cannot tell whether a price is fair until you know the full bill, not just the headline. The one question to ask before you buy anything So before you buy any house, here is the mental upgrade. Most people ask, "Can I afford the loan?" The smarter question is: "Can I afford everything AFTER the loan?" "Can I afford everything AFTER the loan?" Do not just save for the property. Save for the life that comes with it. The fees, the renovation, the furniture, the emergency buffer, the years of instalments. A RM500k house isn't always a RM500k decision, and the buyers who understand that early are the ones who never have to panic-sell later. If you are weighing up a property and want a clear, honest read on the all-in cost for your specific budget and area, a local IQI property agent can help you map out the deposit, fees, exemptions you qualify for, and the realistic monthly commitment, before you sign anything. No pressure, just clarity. Talk to an IQI agent here. Sticker price vs real cost: a quick comparison What you seeWhat you actually plan forRM500,000 house priceRM650,000 to RM700,000 all-in"Just pay the 10% deposit"RM60,000 to RM90,000 in ready cash before keysMonthly instalment looks fineRM320,000 to RM390,000 in interest over the tenureMove in and relaxRM10,000 to RM30,000 in installations and furniture"Stamp duty will kill me"First-timers up to RM500k: exempt until end-2027 A bit of market context (so this isn't just our opinion) To anchor the numbers: stamp duty in Malaysia follows the Stamp Act 1949, with transfer duty charged progressively from 1% to 4%, and a flat 0.5% on the loan agreement. Legal fees are fixed by the Solicitors' Remuneration Order 2023 at 1.25% on the first RM500,000. The first-time buyer exemption for homes up to RM500,000 was extended to 31 December 2027 in Budget 2026. And home loan rates are tied to BNM's OPR, which has held at 2.75% since July 2025. These are not guesses, they are the framework every Malaysian buyer is working inside right now. A quick word from the people who do this daily Here is what experienced agents tend to tell first-time buyers, and it rarely makes it into the brochure: "The clients who stay happy are the ones who walked in already knowing the full number. They did not fall in love with a price, they fell in love with a plan. The ones who struggle usually budgeted only for the house and the loan, then got blindsided by renovation and cash flow in the first year. Buy within your real capacity, keep a buffer, and the home becomes a joy instead of a stress." In short: the house is the easy part. The plan around the house is what protects you. Frequently Asked Questions How much cash do I really need to buy a RM500,000 house in Malaysia? Plan for around RM60,000 to RM90,000 in ready cash before you collect your keys. This covers the 10% down payment (RM50,000), legal fees, stamp duty, and disbursements. First-time Malaysian buyers can save roughly RM11,000 thanks to the 2026 stamp duty exemption, but legal fees still apply. Do first-time home buyers pay stamp duty in 2026? No, if you qualify. Malaysian citizens buying their first residential property priced up to RM500,000 receive a 100% exemption on both the transfer (MOT) and loan agreement stamp duty, for Sale and Purchase Agreements signed between 1 January 2026 and 31 December 2027. The exemption does not cover legal fees. Why does a RM500k house end up costing RM700k? The RM500,000 is only the purchase price. Once you add upfront costs of around RM70,000 (deposit, fees, duty), renovation of RM30,000 to RM100,000, and furnishing of RM10,000 to RM30,000, the all-in figure commonly reaches RM650,000 to RM700,000. Loan interest then pushes the lifetime cost even higher. How much interest will I pay on a home loan in Malaysia? On a RM450,000 loan at around 4% interest, you can expect to pay roughly RM320,000 over 30 years or RM390,000 over 35 years in interest alone. The exact amount depends on your bank, your rate, and your tenure, so comparing loan packages before signing can save you tens of thousands. How can I avoid the "RM500k becomes RM700k" trap? Budget for the total cost of ownership, not just the loan. Save a separate buffer for renovation, furnishing, and at least a few months of instalments. Ask "Can I afford everything after the loan?" rather than only "Can I afford the loan?" A local property agent can help you calculate the realistic all-in number for your situation. Buying soon? Get your real numbers first. Do not let a RM500k house surprise you with a RM700k bill. An IQI property agent can break down your exact upfront costs, the exemptions you qualify for, and a monthly commitment that fits your life, not just your dream. Speak to an IQI property agent today and buy with clarity, not crossed fingers. [custom_blog_form] Continue reading: 4 Essential Agent Fees When Selling a House in Malaysia 2026 Want to Hit the RM500k Mark in Your EPF Savings by Age 60? Here’s Your Guide to It! Starting an Airbnb in Malaysia (2026): A Side-Hustler’s Real-Life Guide Ringgit Strong in 2026: Why Cost of Living and Property Still Feel Expensive in Malaysia Don’t Buy in Dubai Before Reading This: 9 Things Every Foreign Investor Gets Wrong Sources Stamp Act 1949 and Budget 2026 stamp duty updates, Lembaga Hasil Dalam Negeri (LHDN) Solicitors' Remuneration Order 2023, Malaysian Bar First-time home buyer stamp duty exemption (extended to 31 Dec 2027), Ministry of Finance Budget 2026 Overnight Policy Rate and Standardised Base Rate, Bank Negara Malaysia (BNM) This article is for general information only and is not financial or legal advice. Figures are estimates based on publicly available 2026 rates and may vary by bank, lawyer, state, and individual circumstances. Always confirm with a licensed professional before making a property decision.

Continue Reading